My thoughts on what the financial markets did in 2025

As you know, I very rarely talk about investments, the returns of different assets or asset classes, etc. That’s not because those things aren’t important. It’s instead because I feel too many people place too much focus on investing, security selection, chasing returns, going after the latest and greatest shiny object created by Wall Street and so forth. In doing so, many people overcomplicate investing and often end up harming their long-term returns from unnecessary fiddling, tweaking and second-guessing of their portfolios.

For those of you who’ve followed me for a while, you know my views on investing. For the vast majority of people, investing doesn’t need to be any more complicated than a few basic low-cost index funds, maybe some individual bonds and then also having ample amounts of cash and cash equivalents such as things like money market mutual funds, Treasury Bills and CDs.

With that in mind, I feel drawing too much attention to the latest market headlines or investing trends will only serve to distract people from following prudent investing processes.

When it comes to investing, control what you can; your overall allocation across different asset classes, diversification of investment choices, the fees of the investments you choose, the simplicity and efficiency of your overall portfolio and, to some extent, how each of your investments are taxed.

Don’t focus on what you can’t control; guessing what stock is going to be the next big thing, guessing whether small company stocks are going to do better than large company stocks, guessing whether interest rates are going to rise or fall, etc.

Also, you shouldn’t pick investments on what they’ve done in the past. And you shouldn’t continue to hold existing investments based purely on what they’ve done in the past (though obviously pay attention to tax implications of selling things in non-qualified accounts). Instead, you should ideally choose investments based on what you reasonably expect they could or should do going forward.

Just because something’s done well in the past doesn’t mean it will continue to do well going forward. Similarly, just because something hasn’t done well in the past doesn’t mean it can’t do well going forward.

Anyway, I wanted to take a moment to comment on some areas of the financial markets in 2025 that I feel are worthy of giving some reflection on.

And I want to add that a former coworker and I used to joke about people referring to “the market.” We worked in a role at the time where we were actively involved in all sorts of markets; the U.S. stock market, the non-U.S. stock market, the U.S. bond market, the non-U.S. bond market, various derivative markets (i.e. futures, forwards, options and swaps), certain commodity markets, etc.

Technically, a “market” is simply any place – whether in-person or virtual – where buyers and sellers meet to exchange things with one another.

In the financial services world, most people are inherently referring to the stock market when they say, “the market.” But my former coworker and I used to have a running joke where whenever someone asked us what the market is doing, we’d ask them which market? And then also offer up some small, obscure and/or made-up market in response. Such as asking them if they’re referring to the Peruvian sloth pelt futures market. It brought us a chuckle.

Anyway, I bring that up because in this article I’m going to be referring to multiple markets; the stock market (both US and non-US), the bond market, the commodities market and the crypto market. So if you want to know how “the market” did in 2025, hopefully this writing has you covered!

Also, I should add that since I’m writing this before 2025 is actually over, I’m only looking at the prices and returns of things through close of business on December 29, 2025. As of this writing, there are still two more trading days left to the year and things can change.

Before finally getting into it, I must give the disclaimer that nothing in this article is to be viewed as advice on what to buy, sell or hold. Any reference to specific indices or securities is purely for information and reference purposes. Past performance is no guarantee of future results. And nothing written or expressed herein is specific to you or your circumstances. As always, this is all just general education.

Okay, now here’s my thoughts on what the markets did in 2025:

Stocks – U.S.

It was another impressive year for the U.S. stock market, as measured by the S&P 500, which is an index that tracks the performance of the stocks of the 500 largest companies whose stocks trade on U.S. exchanges.

More specifically, I’m going to refer to the returns of Vanguard’s S&P 500 ETF, ticker VOO. Again, this is in no way a recommendation that you should or shouldn’t consider using this particular fund. And there are multiple other funds out there who similarly track the S&P 500. I’m referencing this particular fund simply because it’s one of the larger and more well-known S&P 500 index funds.

And I should note that the returns of the fund won’t be identical to the returns of the S&P 500 itself. You can’t actually invest directly in an index, as it’s just a reference to the returns of multiple other individual securities. But you can invest in an index fund, which seeks to replicate the returns of the underlying index. And, generally speaking, the returns of the fund will be very close to the returns of the actual index. Not identical, but returns will normally be different by only a few hundredths of a percent each year.

Anyway, through December 29, 2025, VOO produced a total return (where “total return” is the return of not just the change in price of the fund, but also the dividends it paid during the year) of +18.9% for the year. And that’s following returns of +24.9% in 2024 and +26.3% in 2023. 2022 was a bad year for the fund, where it lost 18.2%. But the three years prior to that had gangbuster returns of +28.6% in 2021, +18.4% in 2020 and +31.5% in 2019.

This is all a long way of saying the S&P 500 has continued to be blistering hot. Not to say it necessarily needs to crash or stall out, but it appears a cooling off is definitely overdo. However, it’s impossible for anyone to know when the stock market will decline, or by how much.

Also, let 2025 be a reminder that wild things can happen to the stock market in the short-term. If you recall, Trump’s “Liberation Day” sweeping tariff announcements in early-April roiled the markets. And many thought that was the beginning of a prolonged sell off.

However, like many short-term dips before it, the market shook it off in short order and marched on upward.

On April 3, the S&P 500 declined 4.8%. On April 4, it declined another 5.8%. Those two days sparked a lot of panic. And then over the next few days, there were further declines. All said and done, the S&P 500 lost nearly 12% in just four trading days. And as of then, April 8, the index was down 14.9% year-to-date.

But then it reversed course and continued its trend upward. Bringing us to where we are now; up close to 19% for the year.

This just goes to show that you should never make knee jerk reactions to short-term events in the stock market. I’d go so far as to say you shouldn’t even pay attention to the news as it relates to the stock market, as it’s all just noise.

Yes, a 12% decline in four days is pretty dramatic, and will cause some emotional distress for even the most hardened of investors. But what makes for prudent investing is the ability to not act on emotions and instead stick to your investing plan.

Assuming your investing plan, allocation and security selection is good and was done with intention, stay the course. Maybe market declines lead to you having to rebalance your asset mix to account for the lower stock valuations. But even rebalancing should be thought about in advance, so you know when you’re going to rebalance, and why. Don’t randomly rebalance whenever you feel like it or when there is a strong trend in the markets one way or the other. That’s ultimately just speculation.

Stocks – International (i.e. Non-U.S.)

After nearly 20 years of the U.S. stock market summarily trouncing on the collective stock markets of the rest of the world, 2025 finally reversed that trend. And in a major way.

Using the Vanguard Total International Stock ETF, ticker VXUS, as an example, the international stock market is up 32.6% year-to-date; almost double what the U.S. stock market has done.

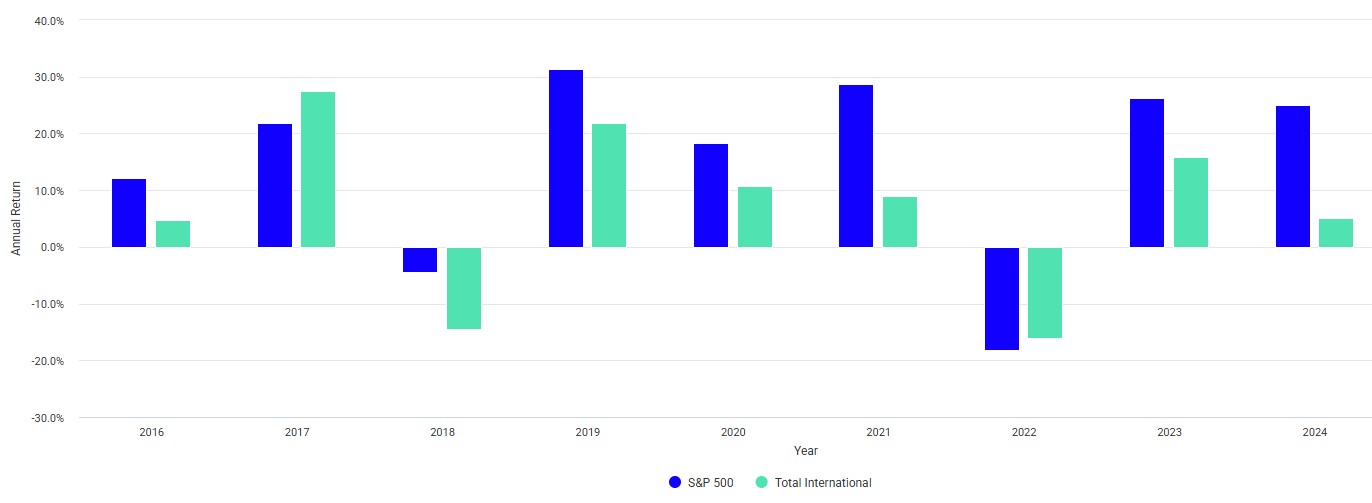

Below are the last nine years of return of VOO vs VXUS, where VOO is in blue and VXUS is in green. As you can see, the returns of the two have trended in the same direction each year. But the U.S. stock market (as measured by VOO) has consistently outperformed the stock markets of the rest of the world (as measured by VXUS).

Even with 2025’s impressive VXUS return of 32.6%, VOO has still outperformed VXUS over the last three, five and 10 years. But 2025 is nonetheless a great example that past performance is no guarantee of future results.

I’ve been beating the drum for years that it’s prudent to consider having a non-trivial allocation of international stocks in stock portfolios; don’t invest solely in the U.S. stock market.

Yes, the U.S. stock market has more or less crushed the international stock market since the Global Financial Crisis in 2008 and 2009. But, for the better part of the decade prior to Global Financial Crisis, the rest of the world’s stock markets performed better than that of the U.S. And my thesis is that even though the U.S. stock market has done markedly better than the international stock market since the Crisis, it shouldn’t be expected that that trend will consistently continue. In other words, there will come a time where the stock markets of the rest of the world collectively perform better than that of the U.S. And 2025 was clearly that time.

Now, always keep in mind that past performance is no guarantee of future results. With that said, it’s possible the U.S. stock market will outperform the international stock market in 2026 and maybe even beyond. So don’t go plowing into international stocks now just because they had a really hot 2025.

Like I said before, don’t invest based on chasing things that have recently performed well. Instead, invest based on what you reasonably expect things could or should do going forward. With that in mind, diversifying stock exposure beyond just the U.S. is a prudent consideration. But how much international stock exposure is the right amount??? That’s largely subjective and will vary across investors if for no other reason than each person will have their own personal views, beliefs and assumptions about things.

Interest rates & bonds – U.S.

I’m calling this section “Interest rates & bonds,” as opposed to just “bonds,” because bonds are ultimately a product whose returns are a direct reflection of interest rates.

For reasons beyond the scope of this article, the price of bonds is really nothing more than a formula that equates all of the bond’s future interest and principal payments to a single present day lump sum value using the market level of interest rates to “discount” all future payments to a current value. And that’s the reason why the price of bonds decrease (increase) when interest rates increase (decrease)…because the price of a bond is nothing more than a mathematical formula whose result is driven by what current interest rates are.

Anyhoo, the two interest rates that arguably matter the most in the U.S. are 1) the yield on the 10-year U.S. Treasury note and 2) the Federal Funds (or “Fed Funds”) rate.

The 10-year Treasury yield started the year at about 4.5%, increased to 4.8% in January, dipped briefly below 4.0% in April (during the Liberation Day stock market selloff) and is currently floating around 4.1%.

Why does this rate matter? Because a large portion of bonds and other fixed income instruments in the U.S. are priced off of the yield on the 10-year U.S. Treasury. And like I said before, when interest rates rise, bond prices decline, and vice versa.

2025’s decline in the 10-year yield is a large part of the reason why total bond market funds did well this year. For example, using Vanguard’s Total Bond Market ETF, ticker BND, as an example, the U.S. total bond market has a year-to-date total return of +7.4%

Specifically, the YTD dividends have been about 4.1%, which means the increase in share price was the remaining 3.3%. Recall it’s total return that matters; not just price return.

If you look at BND’s change in price since the beginning of the year, it will look like the fund is only up 3.3%. But you have to account for the fact that it also paid monthly dividends throughout the year. And those dividends totaled about 4.1%. Which means the total return was +7.4%.

That’s a strong return for a U.S. total bond market fund, where returns fluctuate year-by-year, but historically have averaged low-to-mid single digit percent. The fund’s total returns over the last nine years prior to 2025 have been:

- 2024: +1.4%

- 2023: +5.7%

- 2022: -13.1%

- 2021: -1.9%

- 2020: +7.7%

- 2019: +8.8%

- 2018: -0.1%

- 2017: +3.5%

- 2016: +2.5%

The obvious standout year – and not in a good way – was in 2022 when the fund lost over 13%. That was a rather extreme anomaly of a year, when the 10-year U.S. Treasury yield spiked from 1.5% to 3.9%. The extent of increase in rates during that year led to a sizable decline in the price of BND.

Again keeping the concept of total return in mind, BND paid about 2.1% in dividends during 2022, but its price declined about 15.2%, hence bringing its total return to -13.1% for the year.

My belief is that, over the long-term, the annualized return of a U.S. total bond market fund such as BND should be expected to roughly average out to what 10-year U.S. Treasuries yielded over that time, give or take a bit. But that’s just an educated assumption about how funds like BND should perform. Obviously there are no guarantees (but I’m fairly confident in saying my educated guess shouldn’t be too far off, given how bond prices are ultimately mathematically bound by how interest rates move).

The other main U.S. interest rate to be aware of is the Fed Funds rate. This is the rate that banks lend money to one another on an overnight basis. And it’s the rate that the Federal Reserve directly controls and changes. So when you hear, “the Fed just decreased rates,” it’s specifically the Fed Funds rate that is being referred to.

While the Fed Funds rate doesn’t directly impact you (since you’re not a bank borrowing or lending from another bank), it indirectly impacts most of you reading this.

Specifically, the Fed Funds rate is the benchmark off of which most other short-term interest rates are based. Such as high yield savings accounts, money market mutual funds and U.S. Treasury Bills.

All else equal, as the Fed Funds rate goes up (down), the interest you get on the products I just mentioned goes up (down).

During 2025, the Fed Funds rate decreased from a target upper limit of 4.50% to its current target upper level of 3.75%. And this decrease is the main driver behind why interest rates have decreased in most high yield savings accounts, money market funds and Treasury Bills.

As it stands now, the future direction of the Fed Funds rate is to be determined. It’s widely expected the Fed will continue to lower rates a bit, though at a measured pace. The Fed’s concern is they don’t want to make interest too cheap, thus spurring people to borrow and buy more, thus potentially driving up prices and inflation. So we’ll see how the future plays out and how the Fed responds. But one thing is clear; the days of easily getting 5+% interest on money market funds and Treasury Bills like we did back in 2024 seem to be long gone.

And this begs the question; if we think we know interest rates are going to continue to decline and people will therefore get even lower interest on “safe” principal protected money like savings accounts, CDs and so forth, what is there to do about it???

That depends how much risk you’re willing and able to take, versus just dealing with whatever interest rates you end up getting over time.

For example, if we think short term interest rates are going to decline to like 2% and your cash and cash equivalent accounts are going to have their interest rates keep sliding down, is there something you can do now to get ahead of it? Maybe. But as always, there are no guarantees.

If you’re certain interest rates are going to decline, then in theory it could make sense to reposition some of your money from bank and cash equivalent accounts to something like a total bond fund. Since bond fund prices increase when interest rates decline, you could potentially get a good return from being in a bond fund during a decline in rates.

However, that is fundamentally very different than just sitting in safe principal protected accounts like savings accounts, CDs, money market funds, etc. With a bond fund, there’s the risk of the price declining, instead of increasing. Whereas in principal protected accounts, there is no risk of a price decrease and losing principal value.

As such, you can’t really compare the two and treat them as equal alternatives. One is riskier than the other, but the riskier option comes with the potential (but not guarantee) for better returns. That’s why I said if you want to try to get ahead of a potential decline in interest rates, it depends on how much risk you’re willing and able to take.

And a similar concept applies to owning individual bonds and holding them until maturity; if you know rates are going to decline such that once your current bond matures, you’ll be faced with having to reinvest the proceeds at lower prevailing interest rates, what could you do about it now???

That again depends on how much risk you’re comfortable taking. Again, owning a bond fund (instead of individual bonds) will likely do you well from a return perspective during a declining interest rate environment. But what if interest rates don’t actually decline? Or what if they spike up like they did in 2022? Then that speculative position will have backfired on you and you would have wished you stayed in the individual bonds and just reinvest their proceeds at lower rates when the bond matured.

There is no universally right or optimal answer for how to best deploy your fixed income and cash allocations. There are various options, each of which carry their own pros and cons. And only time will tell what will have ended up the best option…in hindsight.

In my opinion, figuring out the fixed income portion of a portfolio is more challenging than figuring out the stock portion. And that’s because there are so many key decision that need to be made, such as going with individual bonds vs bond funds. Or instead just using cash equivalents like savings accounts, CDs, money market funds and Treasury Bills. Or do you do some combination of these things? And if you use individual bonds, what maturities do you use, and how much money do you put into each maturity???

Commodities – Gold and Silver

I’m not much of a commodities person. I feel they carry a lot of risk and don’t necessarily compliment a broader portfolio as much as some believe they might.

But I feel the need to comment on what a banner year gold and silver had in 2025. And in the case of silver, concerningly good to the point it seems clear a really large bubble formed.

Gold is up 67.4% for the year and silver is up 162.0%. Yes, you read that correctly…+162.0%.

Again, keep in mind that simply chasing returns and investing in what’s done well recently isn’t historically a formula for success. And also keep in mind nothing in this article is to be misconstrued as investing advice; I’m not saying you should or shouldn’t investing in commodities.

I don’t have anything else to add here. I just felt the need to comment on these huge price increases.

Bitcoin

There are many different forms of crypto assets, but Bitcoin is the most widely known, tracked and held. So I figured I’d make a comment about it. Though keep in mind each crypto asset can have dramatically different returns. As such, Bitcoin’s returns are not necessarily representative of the returns of other crypto assets.

For 2025, Bitcoin lost 5.6%. And it had some pretty wild fluctuations during the year. Through October, it was up over 30% for the year. But then it since gave that all back, and then some, resulting in the year-to-date loss of 5.6%.

2025 was a good example of just how risky and volatile crypto assets can be. That doesn’t mean things like Bitcoin can’t continue to have an upward price trend over time. But there can be potentially wild swings in price along the way.

If you’re considering investing in Bitcoin or other digital assets, make sure you have the financial wherewithal (and stomach!) to deal with the risk.

For what it’s worth, my view is that there are equal chances that Bitcoin will continue to increase in price over time, or that it will significantly crash and never recover. I frankly wouldn’t be surprised by either outcome. But I’m admittedly not an expert in crypto.

Well that’s a wrap for my 2025 market commentary. Hopefully you found it informative, if nothing else. And again, nothing in here is investment advice or a recommendation of what you should buy, sell or hold! 😊