Don't compare your portfolio’s returns to those of the S&P 500

If you’re looking to compare the returns of your investment portfolio to the returns of some kind of benchmark, the S&P 500 is almost certainly NOT the appropriate benchmark for you.

Allow me to explain.

First, let’s start with what the S&P 500 is. The S&P 500 (which stands for “Standard & Poor’s 500”) is an index that measures the aggregate value of the stocks of the 500 largest companies whose shares trade on public U.S. stock exchanges.

The S&P 500 does NOT include companies that are privately held and do not have publicly traded shares. For example, Cargill, Koch Industries, Publix Supermarkets, X (formerly Twitter) and Hobby Lobby are large companies that are household names. However, they are privately owned and therefore not included in the S&P 500.

While the index doesn’t capture all of the nearly 3,800 publicly traded U.S. stocks, the returns of the index are nonetheless widely viewed as a proxy for the returns of the whole U.S. stock market. How can that be??? If the index only captures 500 of the nearly 3,800 publicly traded U.S. companies, how is it a good indicator of the whole of the U.S. stock market??? Read on…

The 500 companies in the index are weighted by market capitalization, or “market cap,” which is the size of a publicly traded company. Market cap is the number of shares the company has outstanding multiplied by its share price. For example, if a company has 5,000,000 shares outstanding and its shares currently trade at $100 per share, the company’s market cap is $500,000,000.

Weighting the index by market cap means the returns of the companies with the largest market caps have a larger impact on the value of the overall index, and vice versa.

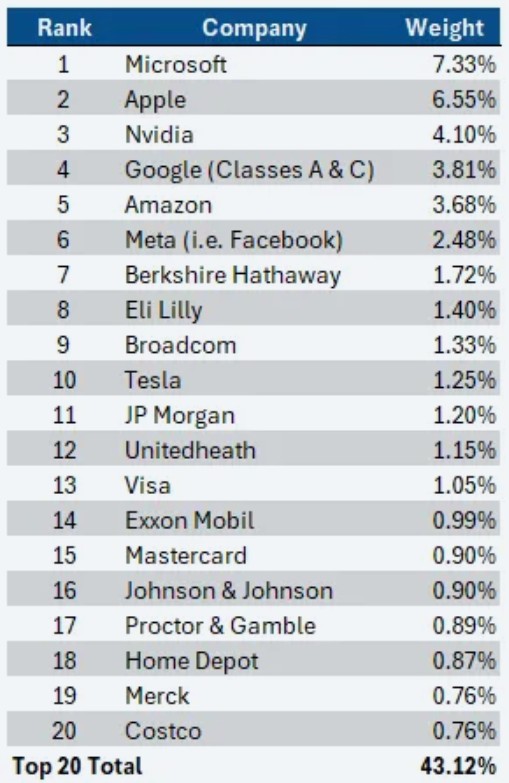

With that in mind, let’s take a quick look at how big the top few companies are in terms of how much of the index they account for:

Here is a summary of the 20 largest companies/ stocks in the S&P 500 as of February 9, 2024. Specifically, it shows how much of the index is comprised by each of these 20:

As you can see, the 20 largest companies in the S&P 500 account for over 43% of the index’s returns. And the heft of the top few names are even more concentrated; the top 10 account for nearly 34%, and the top account for more than 25%!

To the other 480 companies in the index: thanks for showing up. But seriously, the returns of each of those 480 other stocks frankly doesn’t matter too much. 4% of the companies in the index account for over 43% of its returns…

And in case you’re wondering what the smallest/last company is in the S&P 500, it’s currently News Corp whose stock represents just 0.01% of the index.

So, is the S&P 500 really indicative of the whole of the U.S. stock market? Or is it just a measure of the returns of the big tech companies and a small handful of some other companies? I would argue the former.

Just because the S&P 500 is heavily concentrated in its top few names doesn’t mean it’s NOT a good proxy for the whole of the U.S. stock market. It means the U.S. stock market is actually thatconcentrated. Or at least it is when viewing it by market cap, which I feel is the most appropriate way to view it.

There are additional indices that attempt to track the returns of the whole of the U.S. stock market; not just the largest 500 companies. And such indices are also typically weighted by market cap.

There are approximately 3,800 publicly traded stocks in the U.S. However, in looking at the historical returns of such “total stock market” indices, it can be seen that their returns have historically been very close to those of the S&P 500.

For example, below are the last 10 years of returns for Vanguard’s S&P 500 fund (ticker VOO, in blue) vs the returns of Vanguard’s Total Stock Market fund (ticker VTI, in red):

As you can see, the two have tracked each other very closely. And this isn’t a surprise; considering how small the smallest 480 companies are in the S&P 500, the remaining ~3,300 smaller companies in the U.S. are that much smaller and therefore have a nearly meaningless weight in the total market index.

For example, whereas the five largest names in the S&P 500 represent about 25% of the index, those same top five largest names still represent about 21% of the roughly 3,800 companies in the total stock market.

In other words, whether you’re looking at S&P 500 index or the U.S. total stock market index, it’s still largely just the handful of biggest companies that really drive the index’s returns and all of the other stocks are more or less just along for the ride.

In summary, even though the S&P 500 isn’t technically representative of the return of the whole of the U.S. stock market, it practically is. So, it’s fair to say the S&P 500 DOES represent the U.S. stock market. Or such is my opinion.

Okay, now that the lesson on the S&P 500 is out of the way, let me explain why it’s almost certainly not a good benchmark for you to use regarding your own investment portfolio.

As you now know, the S&P 500 represents the returns of the U.S. stock market. It does NOT reflect returns of holding cash or cash equivalents (such as CDs, Treasury Bills, money market mutual funds, etc.). It does NOT reflect returns of holding bonds or bond funds. It does NOT reflect the returns of holding international stocks.

In other words, the returns of the S&P 500 are not indicative of the returns you should expect in your portfolio UNLESS your investment strategy is to invest purely in the S&P 500. For virtually everyone reading this, I’m confident in saying that’s almost certainly not your investment strategy.

Yes, the S&P 500 (or, more generically, the U.S. stock market) is probably a large portion of your portfolio. And, for some of you, it may make up the entirety of the stock portion of your portfolio.

But for people in or near retirement, it’s rarely prudent to invest purely in stocks. And even if you do, it’s not prudent to invest purely in U.S. stocks.

I’m assuming most of you invest in some form of “balanced” portfolio, such a 60/40 allocation where 60% of your investable assets are in stocks and the other 40% are in bonds and/or cash.

Even if the entirety of the 60% of your stock allocation is invested in the S&P 500, the 40% that’s in bonds and cash is not. And the returns of the bonds and cash portion will be very different than the returns of the S&P 500 portion. Sometimes the returns of your bond and cash allocation will be better than the returns of the S&P 500. But many (i.e most) times, they will not.

Therefore, it would be unfair - or at least not meaningful - to compare the returns of your portfolio to the returns of the S&P 500. That would be apples to oranges. Historically speaking, a 60/40 portfolio would have underperformed the S&P 500. But does that mean your portfolio wasn’t invested properly for you and your unique circumstances, or that it didn’t perform well or as expected??? No.

If you do employ a 60/40 allocation to your portfolio, a much more appropriate benchmark would be to look at the historical returns of a fund like Vanguard’s Balanced Index Fund (ticker VBIAX), which is constructed to always have an allocation that’s roughly 60/40. The returns of that fund are MUCH more indicative than the returns of the S&P 500 with regards to what kind of returns a 60/40 portfolio is likely to have produced.

However, even the returns of that fund aren’t a perfect benchmark for most peoples’ 60/40 portfolios. Because what’s to say the mix of stocks in that fund are right - or better for you - than the mix of stocks you have in your own portfolio.

Also, that particular fund only invests in U.S. stocks and bonds. It’s generally prudent to fold in some international diversification to your portfolio.

So, don’t expect the returns of your 60/40 portfolio to precisely track the returns of Vanguard’s Balanced Index Fund. Your returns should presumably more or less follow the same trend as those of the fund. But they certainly won’t be identical. Your returns will sometimes be better, and they will sometimes be worse. But that doesn’t mean your 60/40 portfolio is inherently better or worse than the Vanguard 60/40 fund; it’s just different.

I’d also like to say that for those of you who invest mainly/solely in index funds because you believe in the merits of passive vs active investing, attempting to benchmark your returns to those of any particular index or set of indices is kind of useless in my opinion. Your returns are going to be whatever they’re going to be, based on the allocations and indices in which you chose to invest.

There will be times where your portfolio will do better than whatever benchmark you choose to look at, and there will be times where it does worse. Again, this doesn’t mean your portfolio is any better or worse than the benchmark index, fund or portfolio; it’s simply different.

In my opinion, the only time where comparing the returns of your portfolio to the returns of some benchmark is meaningful is when you (or your investment advisor) is specifically trying to actively manage your portfolio to outperform said benchmark. In this case, only by carefully comparing the returns of your portfolio to the returns of the benchmark will you know if your strategy objective is being met.

In comparison, when your are NOT specifically trying to outperform some benchmark and you’re investing approach is simply to be properly allocated, properly diversified, etc., measuring your portfolio returns vs some benchmark’s returns isn’t going to do anything other than make you continually overthink and question yourself and your portfolio.

In closing, the returns of the S&P 500 represent the returns of the whole of the U.S. stock market. But you should NOT compare the returns of the S&P 500 with the returns of your portfolio.

Sure, it’s an interesting informational exercise to look at the returns of the S&P 500 for the fun of it. But, unless your investment objective is to invest purely in a diversified basket of large U.S. stocks and nothing else, looking at how your portfolio performed relative to the S&P 500 is probably something you shouldn’t do.

Disclaimer:

None of the information provided herein is intended as investment, tax, accounting or legal advice, as an offer or solicitation of an offer to buy or sell, or as an endorsement, of any company, security, fund, or other securities or non-securities offering. The information should not be relied upon for purposes of transacting securities or other investments. Your use of the information is at your sole risk. The content is provided ‘as is’ and without warranties, either expressed or implied. Tenon Financial LLC does not promise or guarantee any income or particular result from your use of the information contained herein. Under no circumstances will Tenon Financial LLC be liable for any loss or damage caused by your reliance on the information contained herein. It is your responsibility to evaluate any information, opinion, or other content contained.