How much Roth conversion to do in a given year

In last month’s post, I discussed seven common scenarios where it could make sense for someone to consider doing Roth conversions. But I said that figuring out the ultimate amount of conversions is far from black and white.

However, while it’s hard to determine a “correct” long-term conversion goal or target, it’s less difficult to figure out how much to convert in any given year. That’s what I’m going to talk about here; what to think about when figuring out how much to convert in a given year.

In reality, this discussion is really more of an explanation of how to do a current year tax return projection, and what to keep in mind when intentionally planning to give yourself additional income. It’s not specific to Roth conversions, per se. But I’ll use Roth conversions as the variable that you’re trying to solve for, based on the other sources of income you’ll have for the year, and the overall tax target or goal you’re trying to hit.

Let’s assume that after reading last month’s post, you decided you want to try to convert a total of $500,000 from your traditional IRA to your Roth IRA. I’m just randomly picking $500,000 as a number for example sake, so don’t get hung up thinking this is a target that you in particular should - or shouldn’t - aim for.

If you’ve been following my content for a while, you likely know that converting $500,000 in one year is probably not the most tax-efficient way to go about it. Chances are, it would be better to spread that over a few years to help minimize spiking your income - and tax rate - in any given year.

But how do you know how much you should convert in a year to make it tax-efficient and not overdo it??? Read on…

When figuring out how much to Roth convert in any given year, there is unfortunately no way around doing a full blown income tax projection for that year. Because unless you know what the rest of your income will be for the year, how can you know how much additional income you can give yourself from doing conversions without making it more tax expensive than it needs to be?

There are various tools to help you do a tax projection. I’m not recommending any over the other, and I’m sure there are more options than what I’m going to mention. But here are a couple that I’m aware of:

- The ”DinkyTown” 1040 calculator. This is a really slick and easy to use FREE online tool. It lets you plug in your various sources of income and shows the total tax amount, including a summary of the taxable income thresholds for each tax bracket.

- TurboTax or other consumer-facing tax prep software. Most (all?) tax prep software not only lets you do your tax return for the prior year, but they also let you do a projection of what your tax return may look like for the current year.

You can use one of the above tools to help you back into how much conversion to do, based on whatever tax goal you’re trying to hit. And in a minute I’ll talk about some of the more common tax goals.

But first, I want to share some thoughts about how to do a tax return projection. Spoiler alert…it can be hard to do, especially with accuracy.

Let’s assume it’s January, and you’re trying to do yourself an income and tax projection for the year to see how much room you have to do Roth conversions.

This will require you to guesstimate - with as much accuracy as possible - all of your sources and amounts of income for the year. Some sources of income will be pretty easy to project. Others will be frustratingly difficult moving targets that are impossible to know with accuracy until much later in the year.

Here are some common items of income and how to try to project them for the year:

- Wages – if you’re working, your compensation is likely to be fixed for the year. If it is, it’s pretty easy to figure out what your total gross wages will be for the year. However, you also need to account for pre-tax adjustments/reductions to your wages, because it’s just the net taxable amount of wages that ultimately flow into your income on your tax return. For example, if you gross $100k of wages for the year but will be making $10k of pre-tax 401(k) contributions, it’s only $90k of taxable wages that will actually hit your tax return and flow into your taxable income.

- Interest – bank account interest is a bit difficult to project with accuracy, as the amount of balances you have in your bank accounts or bank products (e.g. savings accounts, CDs, etc.) can fluctuate throughout the year. Additionally, the rate of interest you get can also fluctuate throughout the year, particularly on things like high yield savings accounts. The best you can do early in the year is make educated guesses about what you think your balances will be for the year, and assume the interest rate will stay the same as it is currently. In reality, these things will almost certainly change, and you’ll likely have to refine your projection later in the year when most of the year’s actual interest has already been paid.

- Dividends – if you own stocks, mutual funds, ETFs, etc. in normal taxable brokerage accounts, you’ll likely have ongoing dividend income throughout the year. Like trying to project interest, projecting dividends for the year requires you to make educated guesses about how many shares of each security you’re going to hold all year, and what the dividend rates will be on each holding. This is another area where you’ll likely have to refine your projection later in the year when most of the year’s actual dividend payments have already happened.

- Capital Gains & Losses – this could be tricky, especially early in the year. You may not currently have plans to sell anything in your brokerage accounts this year. But what’s to say you don’t change your mind for whatever reason in a few months and sell something at a taxable gain, or tax-reducing loss??? This is definitely an area where you’ll have to update your projection throughout the year as actual sale activity occurs, and the amount of taxable gains or losses become known.

- Social Security – this is thankfully pretty easy for most people to estimate. If you already started Social Security, you know how much you get each month. Simply multiply that amount by 12 to figure out the full year of income. And note that it’s the gross amount of Social Security you want to capture on your tax return; not the amount that’s net of tax withholdings or Medicare premium deductions.

- Pensions – like Social Security, this is pretty easy in most cases. If you’re getting a pension, you know how much you’re getting each month. Multiply that by 12 to get to the expected annual amount.

- Taxable distributions from pre-tax accounts like IRAs, 401(k)s, 403(b)s, TSP, etc. – this could be easy…or not. Thankfully you control how much distribution you take from these accounts each year (subject things like Required Minimum Distributions, where you have to take out at least a certain amount). So, in theory, you should know the total amount you’ll be taking out for the year. However, it’s possible that plans change for whatever reason, and you end up taking out more or less than originally planned. Like the other things mentioned so far, you’ll want to revisit your projection later in the year to update and tweak things accordingly.

- Deductions – you’ll have to try to guesstimate what your itemized deductions might be. Or, more likely, chances are you’ll just be taking the standard deduction. In which case that’s easy to know with certainty. But maybe you’ll have other income-reducing things like contributions to a Health Savings Account (“HSA”), a pre-tax IRA contribution, etc.

There are potentially A LOT more things to account for in your income tax projection. But the above few items are the most common. Hopefully this list at least gives you some food for thought and gets you thinking about the other things unique to you that you’ll need to account for in your tax projections.

Okay, now let’s talk about some of the common tax targets or goals to keep in mind when backing into how much Roth conversion to do for the year:

Staying within a certain tax bracket

The U.S. income tax system is a progressive system based on “marginal” income tax rates. Instead of all dollars of income getting taxed at the same rate, the first bunch of dollars are taxed at one rate, the next bunch of dollars after that are taxed at a higher rate, the next bunch of dollars after that are taxed at an even higher rate, etc.

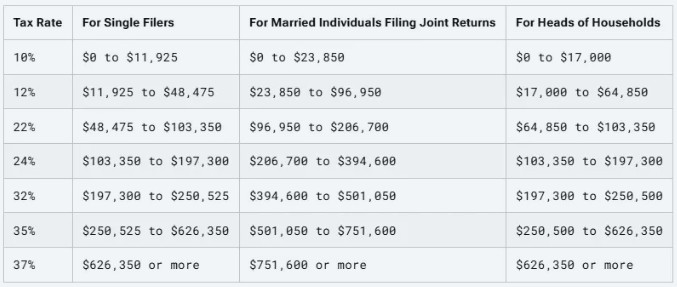

Here are the tax brackets and rates for 2025, courtesy of the Tax Foundation:

As an example, if someone is Single and has $20,000 of taxable income in 2025, the first $11,925 of that would be taxed at 10%. The next $20,000 - $11,925, or $8,075, would be taxed at 12%.

Depending what bracket you’re already going to be in, you might want to limit the amount you convert so that you don’t exceed that bracket. Or don’t exceed a bracket that has a large jump to the next bracket.

For example, if you’re going to be in the 22% bracket due to your other sources of income, you can convert just enough to get to the top of the 22% bracket and stop there. However, there isn’t a big difference in tax rates between the 24% and 22% brackets. So maybe you instead convert enough to not only fill up the 22% bracket, but fill up the 24% bracket. Paying an extra 2% tax isn’t too painful.

On the other hand, going from the 24% bracket to the 32% bracket is a pretty big jump. Paying an extra 8% in tax might sting a little. So you might not want to convert so much that you push your taxable income into the 32% bracket.

However, keep in mind that the tax system is marginal. Even if you do push yourself into the 32% bracket, it’s not like all of your income then gets taxed at 32%. It’s only going to be those incremental dollars beyond the 24% bracket that get taxed at 32%. So it’s not the end of the world if you spill over into the 32% bracket a bit.

Also keep in mind that I’ve only thus far talked about federal income taxes. If you live in a state that has income tax, you’ll also want to factor in the state income tax considerations.

Staying within a certain Income-Related Monthly Adjustment Amount (“IRMAA”) threshold if you’re 63 or older

The amount of premiums you have to pay for Medicare are based on the amount of gross income you have. All else equal, the higher your gross income, the more you have to pay in premiums for Medicare Parts B and D. The additional amounts/surcharges are called Income-Related Monthly Adjustment Amounts, or IRMAA.

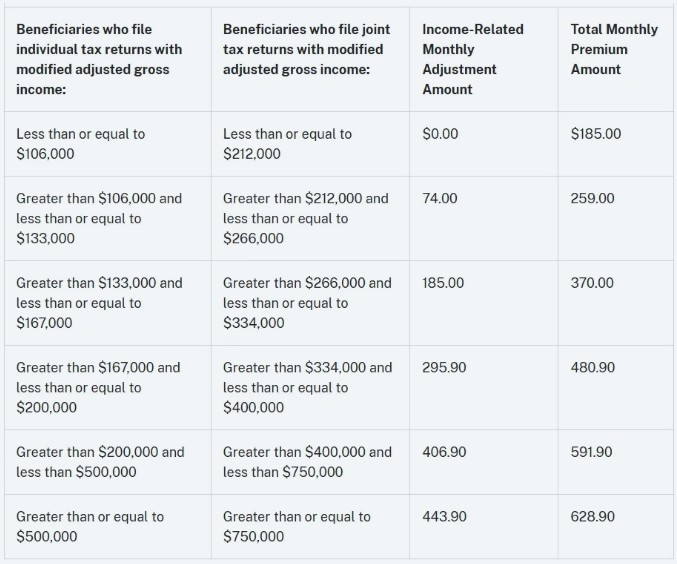

For example, here are the monthly amounts of Part B premiums you have to pay in 2025 based on your gross income from 2023 (yes, you read that correctly…2025 premiums are based on 2023’s income. I’ll talk more about that in a second):

If you’re Single and your gross income in 2023 was more than $106k but less than or equal to $133k, you have to pay $259/mo for Part B in 2025; $74/mo more than the base premium amount of $185/mo.

Technically, the measure of income that’s used for IRMAA is a special measure of Modified Adjusted Gross Income, or MAGI. Specifically, it’s your Adjusted Gross Income off your tax return, plus the tax-exempt interest shown on your tax return.

On the 2023 Form 1040 tax return, Adjusted Gross Income is taken from line 11 and tax-exempt interest is taken from line 2a.

As to why the income measure is two years behind the year of the Medicare payments, that’s because your tax return from two years prior is the most recent tax return available when the Centers for Medicare & Medicaid Services (“CMS”) set the Medicare premium and IRMAA amounts.

The 2025 Medicare premium and IRMAA amounts were determined and announced in late-2024. At that time, the most recent tax returns that people have filed were for 2023. Hence, 2025’s IRMAA amounts are based on income shown on people’s 2023 returns.

And that’s why you need to start paying attention to your gross income starting the year you turn 63. Assuming you start Medicare at age 65, CMS will look to your tax return two years prior (i.e. the year you were 63) to determine your IRMAA amount, if any, when you start Medicare.

Anyway, similar to the concept of limiting conversions to keep your taxable income within a certain tax bracket, some folks limit conversions to keep their MAGI within a certain IRMAA bracket.

I’m not saying IRMAA should dictate your broader income planning. But it’s nonetheless something to take into consideration.

For what it’s worth, I think IRMAA shouldn’t necessarily stop people from doing conversions. Especially if they have a lot of pre-tax money in IRAs, 401(k)s, etc. It should indeed be taken into consideration, but it should not necessarily be the main decision driver.

I feel the first band of IRMAA isn’t too punitive and typically shouldn’t stop people. But when you climb up a few more brackets on the IRMAA scale, then the monthly surcharges start to get chunkier and more noticeable.

But still, it’s impossible to say if paying a few thousand bucks of IRMAA now is or isn’t ultimately going to be worth the long-term tax savings from converting money and having that much less tax to pay in the future on your pre-tax accounts. Like I mentioned in last month’s post, there are way too many unknown variables about the future to know for certain how much long-term tax savings, if any, you’ll get from proactive tax planning and doing things like Roth conversions. Though that’s not to say there isn’t value there.

Minimizing or avoiding the Net Investment Income Tax (“NIIT”)

Many people aren’t aware of a stealthy additional federal tax called the Net Investment Income Tax, or NIIT.

NIIT is an additional 3.8% tax that might be applied to passive sources of investment income such as interest, dividends, capital gains, rental income, etc.

Specifically, if you’re single and your gross income (technically MAGI, but this MAGI is equal to Adjusted Gross Income for most folks) is $200k or more, some or all of your passive investment income may be subject to the extra 3.8% NIIT. And if you’re married and file a joint return, the MAGI threshold is $250k.

There is more to NIIT than this, and the rest of the details are beyond the scope of this post. But I wanted to bring it up so you’re aware it’s something else to fold into the mix of tax planning and doing income/tax projections. If you convert enough to put your MAGI into NIIT territory, you’ll not only have to pay the ordinary income tax on your conversions, but you may now subject some or all of your passive investment income to an additional 3.8% tax. Though to be clear, conversions themselves are not subject to the additional 3.8% tax. But the additional income created by conversions can push your MAGI into NIIT territory such that your passive investment income may then be hit with NIIT.

Managing Affordable Care Act (“ACA”) premium tax credits/subsidies

If you are not yet on Medicare but aren’t covered by employer-sponsored health insurance, you may possibly get health insurance through the Affordable Care Act (“ACA”), aka Obamacare.

Depending on the particular policy you have, where you live and what your gross income is (again, this is technically yet another version of MAGI), you may be eligible for subsidies on the monthly premium amounts you pay for the policy.

All else equal, the lower your income, the larger the subsidies. Which means if you do Roth conversions and increase your income, you will reduce - and potentially eliminate - the amount of subsidies you’re able to get.

Trying to optimize the balance between maximizing ACA subsidies (i.e. minimizing income) and doing conversions (i.e. increasing income) to reduce your longer-term tax obligations is really difficult. It’s another one of those things that’s impossible to nail down with quantitative certainty because there is too much about the future that we can’t possibly know now, such as future tax rates, your taxable income in the future, the returns/growth you’ll get in your various investment accounts (and therefore what your Required Minimum Distributions will be), etc.

However, there is often some “a bird in the hand is worth two in the bush” at play here. If you’re able to get thousands of dollars of ACA subsidies per year for having low income, you may find that more palatable than doing large conversions - and reducing or eliminating those subsidies - for the hope of longer-term tax savings.

I’ll wrap it up here. I’m sure there are other things to consider and different tax targets or goals that people may have when trying to decide how much Roth conversion to do in a given year. But, in my experience, the four things mentioned above are the most common; at least for those of you likely to actually be reading this!