If you're 63 or older, make sure you get to know IRMAA

If you’re within two years of signing up for Medicare, it would be helpful to know who IRMAA is.

No, IRMAA isn’t actually a person. It’s an acronym that stands for Income-Related Monthly Adjustment Amount and it’s a monthly surcharge you may have to pay on your Medicare premiums if your income is over a certain level.

I’ve talked about IRMAA a few times throughout my newsletter and other content sources. However, I feel it’s an important enough topic to bring up every now and again to make sure people have at least heard of it.

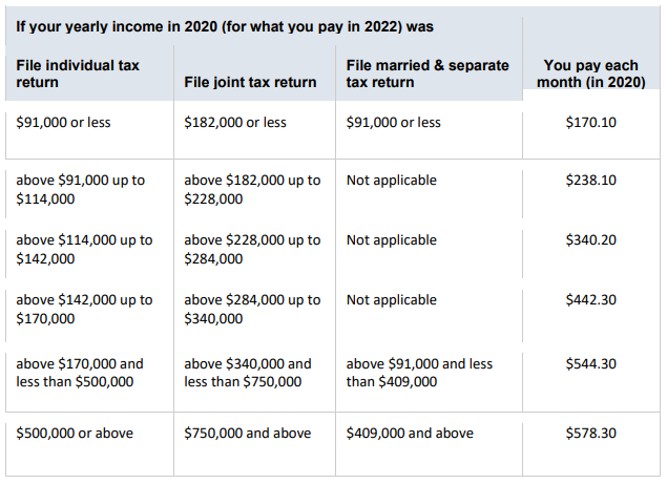

For 2022, the base monthly Medicare Part B premium is $170.10. However, many people pay more than this. Specifically, if your gross incomes in 2020 was over certain levels, you are subject to varying levels of IRMAA surcharges for 2022.

Yes, you read that correctly…IRMAA surcharges you have to pay for 2022 are based on your reported gross income from 2020. There is always a two-year lag between your gross income and your IRMAA, if any.

This is because of the timeline of how the government finds out about your gross income. For example, the 2022 Medicare premium and IRMAA amounts were announced in late-2021. At that time, the most recently available gross incomes reported to the government were those reported in your 2020 tax return (i.e. the tax return filed in early-2021). Therefore, it’s the gross income reported on your 2020 tax return that impacts the Medicare premiums you pay in 2022.

Furthermore, the IRMAA surcharges, if any, you may have to pay reset every year. There is always a rolling two-year income lookback. Specifically, the IRMAA surcharges applicable for 2023 will be based on 2021 incomes, 2024 surcharges will be based on 2022 incomes, etc.

Here is a summary of the various 2020 gross income thresholds and their respective 2022 Part B premium amounts, inclusive of the IRMAA surcharges:

It’s important to know these income thresholds and the respective surcharge amounts change each year, as they’re adjusted for inflation. We won’t know the 2023 IRMAA surcharges or 2021 income thresholds until late-2022.

Also, it’s not just Part B that is subject to IRMAA surcharges; Part D premiums also have surcharges ranging from $12.40 to $77.90 per month (for 2022).

For more information about IRMAA, including when you may be able to get your surcharges waived for certain qualifying life events such as retirement, check out my podcast episode here or my YouTube video here.

In some cases, IRMAA may be unavoidable. However, there are many times where some thorough tax and income planning could help minimize IRMAA. The first step to planning around IRMAA is to fully understand it. Hopefully you find this newsletter, my podcast and my YouTube video helpful!

Disclaimer:

None of the information provided herein is intended as investment, tax, accounting or legal advice, as an offer or solicitation of an offer to buy or sell, or as an endorsement, of any company, security, fund, or other securities or non-securities offering. The information should not be relied upon for purposes of transacting securities or other investments. Your use of the information is at your sole risk. The content is provided ‘as is’ and without warranties, either expressed or implied. Tenon Financial LLC does not promise or guarantee any income or particular result from your use of the information contained herein. Under no circumstances will Tenon Financial LLC be liable for any loss or damage caused by your reliance on the information contained herein. It is your responsibility to evaluate any information, opinion, or other content contained.