Roth conversion analysis: more than meets the eye

There is a lot that goes into deciding if doing Roth conversions might potentially be of benefit. And, unfortunately, the analysis isn’t nearly as easy, objective or definitively knowable as many want to believe it is, or should be.

Roth conversion analysis is something we do regularly at the firm. And the more we’ve done it and tried to solve and optimize as much as possible, the more we’ve realized there are too many future variables that can greatly impact the ultimate benefit – if any – of doing conversions. Each one of those variables can have a meaningful impact on the long-term potential tax savings or cost of doing conversions. And there will be no way to know for sure if conversions ended up being of value, or by how much, until you’re gone from this world. Even then, it’s impossible to pinpoint exactly how much tax you might have saved from doing conversions.

With that said, that doesn’t mean conversions can’t potentially be of value. They could, but we need to realize the math and analysis behind it is much less certain than software and some advisors would lead you to believe.

This article is a summary of a presentation I gave at an advisor retirement planning conference in Orlando last month. The presentation was titled, “Roth Conversion Analysis: More Than Meets the Eye.” Side note: an advisor friend of mine said that title is lame. I don’t disagree! I admit I’m not very creative with things like coming up with presentation titles. But I digress.

The presentation’s goal was to summarize the various areas of analysis that need to be factored into determining if Roth conversion can potentially make sense for someone. In doing so, it would be seen that there are way too many very important variables whose future outcomes can’t possibly be known with certainty. Therefore, trying to quantify and put a number to the tax savings or “value” of doing conversions is really just a big educated guess.

But that doesn’t mean the analysis shouldn’t be done. It just means we shouldn’t get too bogged down in trying to put a number on what we think conversions can do for our tax situation over our lifetimes. What we should instead focus on is what I like to call the “directionality” of whether conversions make sense. It’s more of a “could conversions potentially be of benefit in the future if we assume X, Y and/or Z might happen???” Using the most accurate current info we have, and our best/most educated guesses about the future, we can at least hopefully come up with a yes or no answer to that question.

However, it’s kind of future trying to get much more detailed than that about what a long-term conversion target or goal should be, or what the potential dollar impact of tax savings from conversions will be. But if you decide conversions could potentially be beneficial over the long-term, then you can get more granular and specific year-to-year with how much you convert, as I’ll detail more toward the end of this article.

With that said, let’s get into it!

WHAT'S A ROTH CONVERSION, AND WHY CONSIDER DOING ONE?

I want to start by briefly summarizing what a Roth conversion is. It’s ultimately a form of rollover from a traditional pre-tax qualified retirement account to a Roth qualified retirement account.

With pre-tax accounts, contributions that go into them are generally tax-deferred, meaning the amount contributed gets you a reduction in your gross income for the year of the deduction. Once the money is in the pre-tax account, any growth in the account isn’t taxed along the way. As such, all money in the account is typically not-yet-taxed, hence the name “pre-tax” account.

You normally don’t pay tax on pre-tax accounts until you eventually take money out of them. Simply put, any dollar you take out is treated as ordinary income to you in the year of the distribution. With this in mind, making a contribution to a pre-tax account isn’t a tax deduction, per se. Yes, it lowers your taxable income in the year of the contribution. But you’re not getting rid of the tax; you’re simply kicking it down the road. It’s a conscious decision to defer the recognition of income tax on that money until some point in the future; i.e. when you eventually take money out of the account.

I should add that it’s possible to make a non-deductible aka after-tax contribution to a pre-tax account. That means the money you contribute does NOT have taxation deferred on it. So the contribution doesn’t lower your taxable income that year. Any growth on the money inside the account is still tax deferred and taxed whenever you eventually take money out. But when you end up taking out the contribution - that was already taxed before it went into the account - you don’t pay tax again on that money.

There’s much more to it than this with regards to after-tax contributions and how they eventually come out of pre-tax accounts. But the rest of this article will be speaking only to money in pre-tax accounts that has not yet been taxed. In other words, this article will assume all contributions in pre-tax accounts were indeed tax deferred.

The opposite tax treatment from a pre-tax account is a Roth account. Unlike with a pre-tax account, you can’t defer taxation on money that gets contributed to a Roth account. In other words, there is no current year tax break or income reduction for making a contribution to a Roth account.

However, the upside of a Roth account is that all money, including growth in the account, can eventually come out tax-free if certain rules are met. Specifically, the most common set of criteria that lead to a Roth distribution being “qualified” and therefore free from any taxes or penalties is that 1) the account holder is at least 59 ½ years old and 2) the account was first funded at least five years prior.

The withdrawal rules around Roth accounts are more convoluted and clunky than that, and they’re beyond the scope of this article. But for now, just now that if certain requirements are met, all distributions out of Roth accounts will eventually be completely free from tax and penalties, unlike with traditional pre-tax accounts, where all distributions will eventually be taxed, and potentially subject to penalty if taken out before age 59 ½.

A Roth “conversion” is when you roll or transfer money from a pre-tax account to a Roth account. Since all money that goes into a Roth account needs to have already been taxed, a Roth conversion is generally taxable. That’s because the money in the pre-tax account has not yet been taxed. And again, for money to go into a Roth account, it needs to have already been taxed.

For example, assume you have a $500k pre-tax IRA. And again assume all of the money in there has not yet been taxed (i.e. you don’t have any after-taxed contributions in there). If you were to convert $50k from your traditional pre-tax IRA to a Roth IRA, you will have to include that $50k in your taxable income on that year’s tax return. In other words, you’ll have to pay tax on the $50k conversion that year.

But then like I mentioned above, assuming you don’t take the money out of the Roth IRA until you meet the qualifying conditions, that $50k and any growth on it will all be tax-free at the time.

So why consider doing Roth conversions??? It ultimately boils down to comparing the tax you pay now vs the tax you think you’d otherwise pay in the future. Long story short, if you think it will cost you less in taxes now to convert the $50k than it would to instead let the money sit and grow inside a pre-tax account and take it out and pay tax on it later, then conversions could make sense. And vice versa.

There’s much more to it than that, as you’ll see from the rest of this article. But that’s really the gist of it; are you in a lower tax situation now than you think you will be in the future??? If yes, conversions could end up being of benefit to you. If no, conversions likely won’t end up making sense for you.

But even then, as you’ll read below, it’s not necessarily just you that you’re trying to plan for. Maybe you’re comparing your tax situation now vs your heir’s tax situation in the future (i.e. if/when they inherit pre-tax account from you). Then, your Roth conversion analysis needs to make educated guesses about your heir’s potential future tax profile. And that can involve a lot more guessing than when trying to make guesses about just your own future tax profile. Read on to see what I mean.

THE FACTORS TO CONSIDER WHEN DOING ROTH CONVERSION ANALYSIS

Okay, let’s now get into the various factors that need to be taken into account when trying to decide if Roth conversions could potentially be of long-term benefit. These aren’t in any particular order, other than I’m starting off with the most obvious ones that likely come to people’s minds. And then the next ones after that might be factors that haven’t really been given much, if any, consideration by many folks when doing Roth conversion analysis.

Current vs future tax brackets, rates and deductions

One of the most obvious factors to consider in the analysis of potential Roth conversion value is what federal tax legislation is now and what it might be in the future. Like I said above, the Roth conversion analysis is ultimately an analysis of paying tax now vs paying tax in the future. As such, current and future tax brackets, rates and deductions definitely matter.

We know with certainty what the current year’s tax rates, brackets and deductions are. As such, we can calculate with confidence how much extra tax it will cost to do $X of conversions this year.

But what will tax brackets, rates and deductions be next year? In five years? In 10 years? In 20 years? That’s the challenge.

We mostly know what tax rates, brackets and deductions will be next year. Barring any surprise legislative changes before next year, we know the federal tax rates are 10%, 12%, 22%, 24%, 32%, 35% and 37%. But what we don’t know is what dollar amounts of income each of those brackets will start and stop. And we don’t know what next year’s standard deduction will be. But we mostly know what those things will be. That’s because the tax brackets and standard deduction increase each year with inflation. While we don’t currently know exactly what next year’s inflation increase will be, we can at least make a reasonable guess. Let’s assume 3%, for example. That’s close enough for now. If it ends up the inflation increase is only 2%, that’s not a dramatic difference. And same thing if it ends up being 4%.

But now fast forward. Assume we’re doing this exercise trying to figure out what tax rates, brackets and deductions will be in 10 years, for example. We frankly have no idea what these things will be in 10 years. And we have even less idea what they’ll be in 20 years.

Tax legislation is written in pencil; it’s always subject to be changed. The balance of political power in the country has a lot of sway over the direction and outcome of tax legislative changes. Considering there will be multiple presidential and midterm elections in the next 10 years, the tax code a decade from now can look very different than it does today. It’s likely to change by more than just some annual inflation adjustments along the way.

All else equal, considering how historically low the current federal tax rates are, and how large the national deficit is, I think it’s safe to assume that federal taxes are likely to become more punitive and higher over time. But there is no guarantee of that. Many people said the same thing a decade ago. Yet we’ve since had federal tax cuts, not increases.

Also, the tax rates, brackets and deductions are just one part of the equation of how much tax someone actually pays…

Current vs future income

The amount of tax someone pays is a function of not only tax rates, brackets and deduction, but also how much income they have. Even though taxes might get more punitive in the future, what’s to say a person’s income won’t decrease such that they end up in a lower tax situation in the future than they are now?

A common example of this is someone who’s in the peak of their earning years, in a high income job. Assume someone is making $400k a year in wages, and they’re 55 years old. Depending on whether they’re married or single, what other income they have, what deductions they might have, etc., they are likely in the 32%, 35% or 37% federal income tax bracket. Which means doing a Roth conversion now will cost them 32%, 35%, or 37% in federal taxes, plus any applicable state income taxes.

Let’s assume the person recently read an article that says tax rates have to go up, and so they person feels they should do something about it now as a result. So they think they should do a conversion. However, even if tax rates do go up, they still might be in a lower tax situation in the future.

For example, assume they plan on retiring in a few years. When they do, their income will decrease by $400k per year as they will no longer have wages. Even if federal tax rates do increase, the person would have significantly lower taxable income such that the actual tax rate they pay could be much lower in the future than it is now, even with higher federal tax rates across the board.

Assume all federal tax rates go up 5% across the board. Meaning the 10% rate goes to 15%, the 12% rate goes to 17%, the 22% goes to 27%, the 24% goes to 29%, and so forth. That would be a pretty big increase in taxes on the surface. But in the case of the person in this example, their taxable income would drop dramatically. While they might be in the 35% bracket now, they might only be in the 27% bracket in the future (i.e. what would be the 22% bracket today, but plus the 5% of assumed increase between now and then).

As you can see, the person would be better off NOT converting $50k at 35% now, because they could potentially only be paying 29% tax on that money in the future if they leave it in their pre-tax account and just distribute it out of there later.

And the opposite can also be true; someone could end up having higher income in the future than they do now. A common example of this is someone who recently retired and therefore doesn’t have any wage income anymore. Maybe all they have is some bank account interest and dividend income from a brokerage account. But eventually, they’ll have Social Security income turned on, maybe they’ll have a pension, they’ll eventually have to take money out of their pre-tax accounts, etc. As such, their income now might be the lowest it will ever be for the rest of their life. With that said, if income tax rates do get worse (i.e. higher) AND their income goes up, that will definitely lead to an increased income tax scenario for them in the future vs now. That could mean doing some conversions now – and pulling forward the taxation of income that will otherwise have to be taxed in the future – could potentially make sense.

Current vs future other tax implications

As you can see from above, the amount of tax someone ultimately pays is a function of 1) what the tax rates, brackets and deductions are, and 2) how much income they actually have. But wait, there’s more!

There could be other direct or indirect taxes that come into play now and/or in the future. Common examples, which also need to be factored into the Roth conversion analysis, are:

Income-based Medicare surcharges known as Income Related Monthly Adjustment Amount (“IRMAA”). For those on Medicare, the amount of premiums paid are not just the base Medicare Part B, C or D premiums, but also potentially income-driven surcharges. All else equal, the higher your gross income, the higher your surcharges.

IRMAA is based on your tax return from two years prior. For example, the Medicare surcharges, if any, you pay in 2026 are based on your income as reported on your 2024 tax return. Due to this two-year lag, people who turn 63 or older (and therefore will be 65 or older in two years) need to consider the potential IRMAA impacts of their income and what Roth conversions might do to it.

Someone who’s 61 doesn’t have to worry about IRMAA, unless they’re married, file a joint return and their spouse is 63 or older. But someone who’s 63 or older typically does, assuming they do indeed plan to start Medicare at 65. Which means maybe conversions might make sense to do when you’re 61. But might not make sense if you’re 63 or older

Affordable Care Act (“ACA”) premium tax credits. For anyone who’s not yet on Medicare and doesn’t get health insurance through an employer, a common option for health insurance is to get a policy through the government exchange, otherwise known as the Affordable Care Act, or ACA. One of the benefits of getting a policy through the ACA is that the amount of monthly premium paid for the policy can be subsidized through tax credits if your income is below a certain level. Specifically, the lower your income, the more subsidy/tax credit you might be eligible for (though if your income is too low, you could be forced onto Medicaid).

ACA premium tax credits have a lot of moving parts and nuances, so I won’t get into all of the details here. But the point is, the higher your income, the less subsidies you might be eligible for. With that said, recall that doing Roth conversions increases your income. As such, if you’re on ACA health insurance, maybe conversions don’t make sense, as they can reduce or eliminate any ACA credits you might be getting.

Net Investment Income Tax (“NIIT”). The Net Investment Income Tax, or NIIT, is an additional 3.8% federal tax that applies on various sources of passive investment income such as interest, dividends, realized capital gains, rental income, etc. For single tax filers, if your gross income is over $200k, NIIT will apply to some or all of your passive investment income. For married filing joint taxpayers, the income threshold is increased to $250k.

Since Roth conversions increase your income, they can potentially put you into NIIT territory if you weren’t already. Or even if you’re already in NIIT territory, doing conversions might subject more of your passive investment income to NIIT. Which means things like NIIT are yet another wrinkle to consider in the Roth conversion analysis.

While conversions themselves are not subject to NIIT’s additional 3.8% tax, they might make more of your other income get the additional 3.8% applied. As such, you can effectively think of conversions as potentially indirectly having an additional 3.8% tax on them, above and beyond whatever your normal tax rate is on the amount converted.

How much of your Social Security is taxable. Under current legislation, not all Social Security income is federally taxable. At most, only 85% of Social Security is taxed.

Without getting into too specific details about the formula for calculating how much of your Social Security is taxable, just know that the more income you have across all sources, the more of your Social Security will be included in your gross income on your tax return. Anywhere from zero to 85% of it can be taxable, where the progression between zero to 85% isn’t necessarily linear or easy to calculate without using a tax calculator designed to do the particular formula.

Again keeping in mind that Roth conversions increase your taxable income, the Social Security taxation issue needs to be taken into account. If you’re not on Social Security now but will be in the future, maybe doing conversions can help reduce how much of your Social Security will be taxable in the future, because you’ll have less pre-tax money that will need to eventually be distributed and included on your tax return in the future.

Or vice versa; if you are currently receiving Social Security, perhaps something less than 85% of your Social Security is currently taxable. But if you start doing Roth conversions, that will increase your income and therefore increase how much of your Social Security is taxable. Which means the tax “cost” of doing conversions could be higher than just what your current marginal tax rate is.

Expected account returns

This one is a bit less direct and less easy to see how it plays into the potential long-term benefits of doing conversions. But, at least to some extent, the future returns of your various different financial accounts can impact the ultimate value realized by doing conversions.

Specifically, when taxes on conversions are paid using money from non-qualified “normal” accounts such as bank or brokerage accounts – as opposed to being paid via withholdings from an IRA where the amount withheld means less of the money is actually going from the IRA to the Roth IRA – the potential long-term benefit of doing conversions can be higher.

It’s hard to articulate and show exactly why this is the case, but the gist of it is that there is more money that makes it to your Roth IRA to grow and compound tax-free and less money in your non-qualified account that might not be earning much interest (e.g. excess cash in a checking account) or that might otherwise have an ongoing tax drag and inefficiency (e.g. an index fund whose dividends are taxable each year).

While it’s a pretty technical read to get through, I think Vanguard’s recent white paper about the “Break-Even Tax Rate” on conversions does a great job of detailing why assumed account returns matter in trying to put a number on the potential value of Roth conversions. You can check out the white paper below:

The point of all of this is that future account returns can ultimately impact the value, if any, you might get from doing conversion. Which means depending on what assumptions you make about future account returns, conversions could be more or less compelling for you.

Expected longevity and the “widow(er)’s tax penalty”

How long you end up living can also impact the ultimate amount of tax benefit conversions might have for you. And a prime example of this applies to married couples.

There is something in the industry that’s often called the “widow(er)’s tax penalty.” In a nutshell, when one spouse dies, the surviving spouse’s total income likely decreases, but not necessarily substantially. However, the surviving spouse’s income tax bill will likely go up; potentially by a lot. That’s because a given dollar of income is taxed more heavily for a single person than it is for a married couple.

Federally, the dollar amount of income at which each tax bracket starts and stops is double for married couples than it is for single people. And standard deductions are doubled for married couples compared to single people. Which means, married couples pay less income tax on $X of income than a single person does.

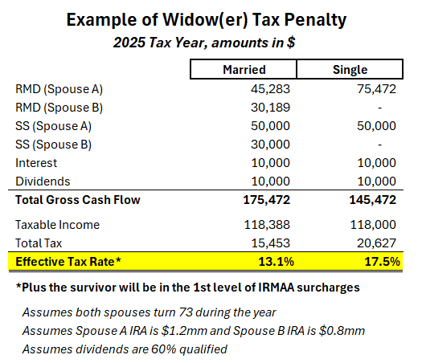

A good example of the widow(er) tax penalty in action is as follows:

- Assume a couple both turned 73 last year, and were therefore subject to Required Minimum Distributions, or RMDs, from their pre-tax retirement accounts

- They have $2,000,000 of pre-tax IRA money; Spouse A’s IRA is $1,200,000 and Spouse B’s is $800,000.

- Spouse A’s Social Security is $50,000 per year, and Spouse B’s Social Security is $30,000 per year

- They have a joint savings account getting $10,000 of interest per year

- They have a joint brokerage account getting $10,000 of dividends per year, where 60% of those dividends are qualified

For 2025, the couple would have collectively had $175,472 of gross cash flow coming into the household. Their total federal taxable income would have been $118,388, on which their total federal tax obligation would have been $15,453. As such, their effective tax rate as a married couple would have been 13.1%

Alternatively, assume Spouse A was instead deceased. Spouse A’s IRA would have likely been left to Spouse B, so Spouse B still would have had the same $2,000,000 of total pre-tax money on which RMDs were required last year.

Spouse B’s Social Security would have stepped up to the $50,000 of Social Security Spouse A was getting, and Spouse B’s $30,000 of Social Security would have essentially fell away.

Spouse B owned the same amount of bank and brokerage assets as when Spouse A was still alive, which means Spouse B would have had the same $10,000 per year in interest and $10,000 per year in dividends.

All said and done, Spouse B (as a single person) would have had only $145,472 of gross cash flow coming into the household. This is $30,000 less than what the household brought in when Spouse A was still alive. Spouse B’s total federal taxable income would have been $118,000; only $388 less than what it was when Spouse A was still alive. Spouse B’s total federal tax obligation would have been $20,627; over $5,000 HIGHER than what it was when Spouse A was still alive. All said and one, Spouse B’s effective tax rate as a single person would have been 17.5% compared to the 13.1% it was when Spouse A was alive. This is the widow(er)’s tax penalty.

AND, Spouse B would now be in IRMAA surcharge territory on Medicare, whereas they weren’t when Spouse A was still alive.

That was a lot of words and numbers I just threw at you. Here it is summed up in table format:

With this in mind, for married couples, doing Roth conversions can help ease the tax burden for the eventual surviving spouse, assuming one spouse eventually predeceases the other. And, all else equal, the sooner the first spouse passes, the more potential tax savings conversions could have, because the surviving spouse would be in the condensed tax brackets and standard deduction as a single person for longer. But obviously none of us know exactly when we’re going to leave this world. So it makes it hard to figure out exactly how much value conversions might have in helping reduce the widow(er) tax penalty in the future.

Legacy goal and priorities

When doing tax planning, you also have to give consideration to who you’re tax planning for. For example, are you trying to minimize taxes for you while you’re alive? Or for your heirs with regards to money of yours they’re going to end up getting after you’re gone? Maybe doing Roth conversions won’t clearly benefit you while you’re alive, but it could eventually benefit your heirs.

For example, assume you’re retired and in the 22% tax bracket. And assume you have more pre-tax money than you will need to use. At one extreme, maybe you have enough pension and Social Security such that those two income sources cover ALL of your expenses. Therefore, any money you have in your retirement accounts will eventually go to heirs.

And further assume you’ll be leaving all of your money to your adult child who’s a really high earner and likely will be for the rest of their life. Assume they’re in the 37% bracket and will presumably always be in whatever the highest income tax bracket is.

Knowing that your child is going to end up inheriting your pre-tax money and, at least under current regulations, they will have to distribute and pay tax on the entirety of that account within 10 years, it could make sense for you to do conversions.

Again, this wouldn’t directly benefit you, but it could lead to your child ultimately being able to get or keep more of your money, net of tax. The basic analysis is that if you convert now at 22%, the amount converted will go into a Roth account that your child won’t have to pay tax on distributing when they inherit it. On the other hand, if you don’t convert now, any pre-tax money you leave to your child will be taxed at your child’s tax rate of 37% (or whatever it might be at the time). All said and done, it would be cheaper for you to 22% pay tax on the money via conversions than it would be for your child to pay 37% tax on the money if you don’t convert it. In that sense, conversions can create a more tax-efficient wealth transfer process.

And the opposite scenario can lead to different results. Assume you’re still in the 22% tax bracket and won’t need any of your pre-tax money while you’re alive. But now assume your child is a starving artist and likely always will be. Therefore, your child is currently in a lower tax bracket than you, and you assume they always will be. In this case, it would be more tax-efficient to leave pre-tax money to your child and let them pay tax on it, instead of you paying tax on it now by converting it.

Another bit to consider here is the qualitative aspect of leaving a legacy. Even if the math isn’t as obvious as in the examples above, maybe you want to get taxes out of the way on your money now while you’re alive, instead of leaving it for your eventual heir to worry about.

Going back again to the same example above where your child is a starving artist and likely always will be, it doesn’t objectively make sense on the surface for you to do conversions now if you know your pre-tax accounts are going to be left to your child for them to pay taxes on. But, maybe you care less about the pure math of the analysis and want to leave your child all Roth money so that they simply don’t have to worry about paying tax on it. Even if it means they’re ultimately getting less, net of tax, by you doing conversions and paying tax now. You might be prioritizing the notion that all of the money your kid gets from you will not be taxable to them. If that’s what’s of higher importance for you, then that’s the right answer for you.

Charitable intent

This one is kind of similar in concept to the point above about legacy desire. Except that it would be a charity receiving your money instead of a child. And charities don’t pay tax, so they’re always in the zero percent tax bracket.

If you’re charitably inclined, you might not want to convert away much, if any, of your pre-tax balances. While you’re alive, you can give away up to $111,000 per year (as of 2026; the figure goes up each year with inflation) directly out of your IRA to a qualified charity, if you’re at least 70 ½. This is known as a Qualified Charitable Distribution, or QCD. The benefit of doing QCDs is that the amount of the QCD that leaves your IRA doesn’t count as gross income on your tax return. Furthermore, QCDs can take the place of RMDs. So if you’re of RMD age and don’t actually need the money in your IRA, you can satisfy your RMD for the year by giving it away as a QCD.

If you know you’re going to be charitably inclined throughout retirement, you can do most or all of your charitable gifting through QCDs, without it impacting your tax return at all, and with also satisfying your RMD each year. With that in mind, doing conversions and paying tax on money from your IRA that you wouldn’t otherwise pay tax on might not make sense.

Similarly, you also need to consider charitable intent after you’re gone. Specifically, if you’ll be leaving large amounts of money to charities after your passing, it would be good to leave them pre-tax retirement account money. Since charities don’t pay taxes, they won’t have to pay tax on inheriting your IRA, for example. Whereas non-charities (like family and friends) DO have to pay tax on inherited IRAs.

If you know you’ll be leaving large amounts of assets to charities after you’re gone, maybe conversions don’t make sense. Or at least, don’t convert money you plan on leaving to charities. Knowing that charities won’t pay tax on any money they inherit from you, you wouldn’t want to pay tax now to convert IRA money to a Roth IRA, just to end up leaving that Roth IRA to charity. The charity wouldn’t have paid any tax even if you left them your IRA. But now you have less to leave them because of the taxes you paid on doing the conversion.

State income tax considerations

Many people mistakenly overlook state income tax considerations when doing tax planning. Federal tax implications rightfully deserve the priority in most cases, because they’re usually more impactful than state implications. But nonetheless, state income tax implications can have a meaningful impact on Roth conversion analysis.

For example, if you’re in a high income tax state now, like California, and plan on retiring to a no income tax state in a couple of years, it might not make sense to do conversions now. All else equal, when you redomicile to the new state, your federal income tax scenario won’t be any different, but your state income tax scenario will be. If you convert now while a resident of California, you’ll have to pay federal AND California income tax on your conversion. But if you wait until you move to the new state to do your conversion, you’ll only have to pay federal income taxes on your conversion.

Depending what state you live in and what amount of income you currently have there, the state income tax differential can be quite large. Using California again as the example, a single person with only about $75k of taxable income is in the 9.3% state income tax bracket. That’s a high state income tax rate for a relatively small amount of income. If that person waits to convert until they move to no income tax state, for example, they will save themselves 9.3% state income tax on the conversions. That’s a pretty big difference.

Different states have different income tax structures to take into consideration when doing Roth conversions analysis if/when you plan on moving. Some states don’t have any income tax (e.g. Florida, Texas, Nevada), some states do have income tax but exempt some or all retirement income - including conversions - from being taxed (e.g. Illinois, Pennsylvania), and some states tax conversions and have fairly high tax rates (e.g. California).

The takeaway here is that if you know you’ll be changing states in the near future, factor that into your Roth conversion analysis. Maybe that will lead you to want to speed up and or do larger conversions, or maybe it will lead you to want to do less or no conversions for now.

Peace of mind or “hedge” value

For some people, there is a lot of intangible value in doing conversions. Even if you can’t necessarily cook up a scenario of future assumptions where conversions will objectively make sense and save on taxes, that’s not to say there isn’t still value in doing conversions.

Some folks get a lot of peace of mind and sleep better knowing they have more of their money in Roth accounts, where they theoretically don’t have to worry about that money being taxed again (barring future tax legislative changes that might change things). Which means they might find value in paying 32% (or whatever rate) in taxes now on doing conversions to not have to worry about what taxes might otherwise be on that money in the future if they didn’t convert. And for some people, that intangible subjective “sleep well at night” benefit is invaluable.

But for other people, they could care less about intangibles like that. They will want to boil everything down to a numerical analysis. In which case, peace of mind value might not be of any value to them at all!

Also, having money spread around different buckets of taxability can act as a “hedge” against the future unknowns of tax legislation and life. Regardless what happens to your tax situation in the future, if you have different choices of what account types to pull your money from, you’ll have more control over your taxes in the future. Having 100% of your money in pre-tax accounts gives you no hedge; every dollar that comes out will be taxed at whatever rates are at the time.

But if you have a decent amount of your money in Roth accounts, for example, then you can later choose to pull some money out of pre-tax accounts and pull the rest out of Roth, where the Roth portion won’t be taxable. So regardless what happens to taxes in the future, you’ll have more control around how your money is taxed. That’s a hedge against future tax unknowns. Again, some people place a lot of value on the idea of having a hedge against future what-ifs, other people don’t. Which means different people might view conversions as having more or less potential benefit than others.

PULLING IT ALL TOGETHER

If you’ve read this far, you might feel like I’m saying a lot without actually saying anything! And that I’m basically saying it’s impossible to put a defensible and accurate numerical figure on how much Roth conversions to do, if any. Because the potential value of conversions isn’t feasible to figure out due to all of the different factors that play into it, and how the outcomes of most of those factors are impossible to know. And this would be true…this IS what I’m saying!

But that doesn’t mean I’m saying people shouldn’t consider conversions. Instead, my views on conversions are as follows.

First and foremost, Roth conversions are a potential optimization technique. Meaning whether you do conversions or not is not going to make or break your overall financial plan. If your financial plan is strong, not doing conversions isn’t going to all of a sudden make your plan bad. And if your plan is not feasible to start with (e.g. you want to spend $200,000 per year for the next 30 years but only have $500,000 from which to spend), doing conversions isn’t going to magically make your plan work.

Doing conversions could potentially make a good plan a bit better. Or they can potentially make a bad plan a little less bad. But again, they are not going to make or break a plan regardless. So don’t dwell too much on any of this if you don’t want to or don’t feel like you can make sense of any of it.

Next, there is planning software that will do this analysis for you. BUT, its results are going to be wrong. Commercial financial planning software operates by necessarily making assumptions about all of the big important future unknowns that I’ve been talking about. And it will then project some very specific number with regards to how much lifetime tax savings Roth conversions MIGHT have for you. But that’s wrong. Maybe you’ll end up realizing more tax savings than that, or maybe it will be less. Or, maybe it will end up in hindsight that conversions didn’t actually make sense and ultimately cost you more lifetime taxes than you needed to pay!

You’ll never actually know the definitive quantitative result of all this until after you’re gone. And even then, there is no feasible way to know for sure how much tax impact conversions had for you unless you carefully tracked two different scenarios over your whole life: 1) what your actual total taxes were during your life vs 2) what your hypothetical total taxes would have been over your life. Most people don’t track #1 as it is. And even less people, if any, actually attempt to track #2.

I firmly feel there is truly no way to know for sure what the ultimate dollar impact of doing conversions – or not – is going to be. Because it’s impossible. Yes, software attempts to do it. But again, software is just making a bunch of guesses about the future. Most or all of those guesses will be wrong to some extent.

However, that doesn’t mean it’s completely hopeless to try to do any sort of meaningful analysis of whether or not doing conversions could potentially make sense. I know there is no way to accurately or honestly come up with a hard dollar figure of the eventual tax savings, or lack thereof, of doing conversions. And there is therefore no way to definitively know how much conversion to do over a lifetime. But, there are at least ways to try to get the directionality right of whether conversions might make sense.

Directionality means signs point to believing something is likely to be of value. While you might not be able to quantify exactly how much something might be of value (e.g. there is no way to definitively put a number on how much lifetime taxes you will save from doing conversions), there are more reasons than not to say something is likely to make sense. This is my approach to giving guidance on conversions.

For example, if someone doesn’t have a lot of pre-tax money, then conversions aren’t likely to be of a lot of benefit, and vice versa. Having $300,000 of pre-tax IRA money isn’t a massive amount of tax-deferred assets to have to worry about future tax impacts on. But having $3,000,000 of pre-tax IRA money is a different story. Which means, directionally speaking, considering conversions could make more sense for someone with $3,000,000 of IRA money vs someone with $300,000 of IRA money.

Another directional example is married couples vs single people. As I showed before with the case of the widow(er)’s tax penalty, conversions could make more sense for married people than single people, all equal, because the married people are in a more favorable tax situation now than they will be if/when one spouse predeceases the other. As such, converting some money now while married could mean paying less tax on pre-tax money than it would if you don’t convert and instead wait for that money to be taxed in the hands of the surviving spouse when they will be under single tax brackets and rates.

Another prime example of directionality is if someone has a lot of income now but won’t in the future. Such as a worker in their highest earning years who will be retiring in a couple of years. Directionally, it doesn’t make sense to convert now when their income is already really high if you know their income will be substantially lower in a few years. And vice versa; someone with low income now that will have high income in a few years might directionally benefit from doing some conversions now as opposed to waiting when their income is higher later.

Folks with strong desires to leave money tax-free to heirs could be good candidates to consider doing conversions. Like I mentioned in a prior example, even if the person is in a comparatively higher tax bracket than their eventual heir will be, they might prioritize the idea of their heir getting money that’s completely tax-free to them. In this case, conversions directionally make sense, even though we can’t necessarily quantify the value or tax savings, if any.

If you’ve decided conversions directionally make sense, then it’s time to decide how much conversions to actually do. While I’m of the view that it’s essentially impossible to precisely know how much to convert long-term, I feel like once you decide that you believe conversions can make sense for you, it’s then a year-by-year analysis of how much to convert in any given year. So don’t feel like you need a big picture multi-year conversion target in mind. Because that might make you feel like you’re spinning your wheels not being able to get to a “right” answer.

Instead, focus on trying to solve for figuring out the conversion amount in any given year, as that’s a lot easier to be more specific on, based on whatever it is you’re trying to solve for that year.

For example, maybe your income is such that you’re already in the 24% federal tax bracket. And maybe you’re not yet 63 or older, so Medicare IRMAA doesn’t come into play yet. So perhaps you decide you want to fill up the 24% bracket with conversions. After all, since you’re already in the 24% bracket, your tax rate on conversions won’t be any incrementally higher than it already is, so it could be a logical view to make the most of the bracket you’re already in and fill it up.

So then you’d need to do some calculations or use tax projection software to figure out how much room you have to add conversions into your gross income, without your taxable income exceeding the 24% bracket. But even if you do accidentally go over and get yourself a bit into the next bracket, which is 32%, it’s not the end of the world. That doesn’t mean ALL of your conversions will then be taxed at 32%; just the portion that’s greater than the 24% bracket will be taxed at 32%.

Another possible limiting factor to doing conversions in a given year is Medicare IRMAA considerations, if you are 63 or older that year. Then, maybe instead of filling up income to stay below a certain tax bracket, you fill up income to stay below the income thresholds where IRMAA would start. Or maybe let yourself get into the first income band of IRMAA surcharges, but not the higher and larger surcharge bands beyond that.

Or if you’re on Affordable Care Act insurance and getting premium tax credit/subsidies because your income is fairly low, you might not want to jack up your income too high and make you ineligible for any credits. So perhaps you convert enough just to fill up your income before you lose premium tax credit eligibility.

Or maybe if you’re 65 or older, you might want to keep your gross income below the level at which you’d be phased out from getting the new temporary senior bonus deduction, which can be as high as $6,000 per person.

And there could be other targets or goals you’re trying to hit or stay under with regards to income. Whatever your priority or income goal is for the year, that can be the governing factor of how you back into how much room there is to do conversions that year.

Again, don’t sweat feeling like you need to try to convert two million dollars over the next 10 years. Who knows, maybe that’s your plan and you want to stick to it. But I suspect for most of you reading this, that’s a bit lofty and unrealistic of Roth conversion goal.

Instead, focus on getting the directionality right; i.e. do you feel conversions can potentially be of value for you, given your long-term planning priorities, guesstimates of tax legislative changes, guesstimates of how much income you’ll have in later years, guesstimates of when you and/or your spouse might pass, your level of charitable intent, and so forth.

Easy, right?! 😊

Disclaimer:

None of the information provided herein is intended as investment, tax, accounting or legal advice, as an offer or solicitation of an offer to buy or sell, or as an endorsement, of any company, security, fund, or other securities or non-securities offering. The information should not be relied upon for purposes of transacting securities or other investments. Your use of the information is at your sole risk. The content is provided ‘as is’ and without warranties, either expressed or implied. Tenon Financial LLC does not promise or guarantee any income or particular result from your use of the information contained herein. Under no circumstances will Tenon Financial LLC be liable for any loss or damage caused by your reliance on the information contained herein. It is your responsibility to evaluate any information, opinion, or other content contained.