Summary of the 2025 Social Security Trustees Report

Every year, the Board of Trustees of the Social Security system puts out a lengthy annual report about the system. In the report, it summarizes the most recent year’s financial operations, as well as long-term projections about the anticipated financial health (or lack thereof) of the system.

For those who’ve never read it, I highly recommend it. Here is a link to 2025’s report, in all of its 282 pages of glory! Obviously reading nearly 300 pages – many of which are filled with detailed charts, graphs and tables of data – isn’t very realistic. But I implore you to at least read the first ~30 pages of “Overview” section as it’s highly informative. If nothing else, it provides a tremendous level of insight into how the system functions and what its comings and goings of money are.

The official name of the report is “The 2025 Annual Report of the Board of Trustees of the Federal Old-Age and Survivors Insurance and Federal Disability Insurance Trust Funds.” But for simplicity sake, I’ll just call it the “Report” going forward.

Before getting into summarizing what’s in the Report, I want to briefly summarize the structure of the system, as that will give more context to better understand the terms and info thrown around later.

What Social Security is and isn’t

At a high level, Social Security is a social welfare system; it is not a savings account or investment account set up for each individual. In other words, it’s not like all the money you pay in is held or earmarked just for you to eventually get back.

When I say it’s a social welfare system, the best analogy I can give is that of paying property tax on your house. In most towns, particularly those that aren’t 55+ communities, property taxes go largely to pay for the town’s public schools. And to a lesser extent police & fire services, waste collection and other municipal services.

But, in looking just at the portion of property taxes that go toward paying for public schools, it’s not like the amount you pay is held and applied specifically for or toward you.

For example, assume your property taxes are $10,000 per year and half of that, or $5,000, goes toward funding public schools.

Whether you have 10 kids or no kids attending the public schools in your town, you’re still paying $5,000 per year toward public schooling. And the longer you live in the town, the longer/more you pay.

Granted, I know people typically don’t enjoy paying property taxes. But I think most folks understand how property taxes work, what the money is used for and how much they do or don’t directly benefit from the taxes they pay. And, generally speaking, I don’t think people feel overly cheated when they don’t have kids in public schools, yet pay as much for public schools every year as their neighbor who has four kids in the schools yet pay a similar amount of property taxes.

On the other hand, with Social Security, many people view it more as their own personal account, where they feel the money they paid in is theirs and they should get more out of it than others who paid in less. That’s not the case. Or at least, it won’t always be the case. Some people get substantially more out of the system than they paid in, others get substantially less than they paid in. And some people get literally nothing out of the system! I’m not saying that makes the system good or bad. I say this just to try to get the point across that it’s ultimately a form of social welfare. And like any form of social welfare system, its structure, fairness and what people get out of it vs what they pay into it will always be hotly debated.

Overall structure of the system

Okay, now for some more specific info about the Social Security system.

The system is made up of two main parts or programs:

- the Old-Age and Survivors Insurance (“OASI”) program

- the Disability Insurance (“DI”) program

The OASI program provides monthly benefits to retired workers, their families and survivors of deceased workers. This is the system that pays the retirement benefits we’re all aware. When people in or near retirement say they’re starting their “Social Security,” they’re technically referring to their benefits from the OASI program.

The DI program provides monthly benefits to disabled workers and their families. If you get hurt, can no longer work and start receiving Social Security disability benefits, those are technically coming from the DI program.

While the two program are technically separate and distinct within the system, they’re often informally combined and referenced as one collective Old-Age, Survivors and Disability Insurance, or “OASDI,” program.

Where money comes from, and where it goes

The system is funded primarily from payroll taxes. Specifically, the vast majority of people who work in the U.S. have to pay a portion of their earnings into the Social Security system. They also additionally have to pay into the Medicare system, but I’ll leave that topic for another day.

Notice I said the “vast majority” of people who work have to pay into the system. Some jobs – specifically some people who work for public state or municipal employers – aren’t actually part of the Social Security system and therefore don’t have to pay into the system. Generally speaking, since they don’t pay into the system, such folks aren’t entitled to receive any Social Security benefits of their own. However, they may be able to receive survivor benefits from a deceased spouse, assuming that deceased spouse was eligible for Social Security benefits based on their work history. But that’s beyond the scope of this article.

The amount of taxes people have to pay into the Social Security system is based on what their earnings are. Every employee pays in the same 6.2% of their earnings, and every employer similarly pays another 6.2% of that employee’s earnings. But, the amount of earnings on which that rate applies is capped.

For 2025 only the first $176,100 of gross earnings are taxed for Social Security; the employee pays 6.2% of their wages (up to that limit), and the employer pays another 6.2% of those wages (again up to that limit).

The wage limit is increased for inflation each year, and therefore increases over time.

For self-employed folks, they’re both the employEE and employER, which means they pay 12.4% in Social Security tax, up to that year’s earnings limit.

To a much lesser extent, the system is also funded from interest received on money held inside the Social Security trust fund (more on that later), and from the portion of federal income taxes attributable to peoples’ Social Security retirement benefits.

That’s about it for how the system is funded, and where its money comes from.

As for how the money is used and where it goes, the vast majority of expenses or outflows of the Social Security system are for benefits paid to retirees, their families, people who are disabled, their families, and survivors of deceased workers.

To a much lesser extent, the system also has some overhead and administrative operational costs, and a small portion of it is also used to fund certain railroad retiree benefits that aren’t technically the same “normal” Social Security system as we know it. I frankly don’t really know much about the whole railroad retiree benefit system, so I can’t expand much else on it.

As for the rules around how and when people can claim Social Security, how and when their families can also get benefits, when people can get disability benefits, etc. that’s all rather complicated, involved and beyond the scope of this article. Also, I’ve covered those topics in other articles, podcasts and videos. So I won’t get into all of those details and strategies here.

However, if you’re interested in some of the previous content I’ve created about claiming Social Security benefits, check out:

- Podcast Episode #025 Introduction to Social Security

- My YouTube video Introduction to Social Security

- June 2024 Newsletter on The Optimal time to claim Social Security

- My YouTube video When to start Social Security

- November 2022 Newsletter on Boosting your Social Security

- My YouTube video Calculating your Social Security Primary Insurance Amount

- My YouTube video Social Security myths and Q&A

How the trust fund works

A final thing I want to share before getting into the specifics of this year’s Report is a very basic overview of how the system’s cash flows function and how the trust fund(s) comes into play (each of the OASI and DI systems has its own trust fund, but they’re also often informally referenced as one combined trust fund).

At a very high level, think about the income and expenses of the Social Security system like a person’s income and expenses; money comes in and money goes out. To the extent more money is coming in than going out, the excess gets saved. But if there is less coming in than going out, those savings have to be tapped to cover the deficit.

For example, assume someone brings in $5,000 per month from wages. To keep things simple, exclude any income tax considerations; just pretend there is $5,000 coming in each month.

And assume their monthly living expenses are $4,500. That means there is an extra $500 of cash coming in for the month. Assume the person puts that into a savings account such that there is now $500 in that account.

And then next month, the same thing happens; the person brings in $5,000 and spends $4,500, resulting in an extra $500 that goes into the bank account. Which means the bank account has now increased to $1,000 total.

Fast forward a few years and assume the same level of income and expenses happened each month such that the bank account has since built up to $12,000.

Then assume the person’s living expenses increase from $4,500 a month to $5,500 a month. However, assume they’re still only bringing in the same $5,000 a month.

This means the person’s monthly cash flow is a $500 deficit, as they’re now spending $500 per month more than they’re bringing in.

In order to cover that deficit, the person takes $500 from their bank account. Which means the bank account decreases from $12,000 to $11,500.

And then assume this persists for the foreseeable future; the person brings in $500 less each month than their expenses. So they keep taking $500 out of their bank account every month to cover it.

So long as there is enough money in “reserves” in the bank account, the person can keep funding the monthly cash flow shortfall. But, if the monthly deficit continues to persist, eventually the bank account will run out.

At that point, one of two things – or a combination of the two things – needs to happen: 1) the person needs to start spending less and/or 2) the person needs to start bringing in more money.

At a very high level, the Social Security system works the same way; money comes in from 1) payroll taxes, 2) income tax on benefits and 3) interest earned on money in the system’s trust fund (where the trust fund is synonymous with the bank account in the above example), and money goes out from 1) paying benefits, 2) paying administrative expenses and 3) paying the railroad retiree benefits.

If more money comes into the system than goes out, the excess goes into the trust fund and gets invested in U.S. government bonds. But, if less money comes into the system than goes out, money is taken out of the trust fund to cover the deficit.

Summary of Social Security’s 2024’s financial results and projections (finally)

Okay, let’s now get into the summary of the Social Security system’s financial operations for 2024, and the Report’s short-term and long-term financial health projections for the system.

The quick takeaway from the Report is that the system is currently paying out more than it’s taking in and is projected to do so for the foreseeable future, unless changes are made to the system. Which means the trust fund is expected to eventually deplete. Specifically, it’s projected that will happen in less than 10 years from now. What would be the ramifications if that were to happen??? I’ll get into that in a bit.

Recall the Social Security system is technically two different systems, each with their own trust fund: the OASI and the DI systems, as previously mentioned.

I bring this up because the Report and news headlines you may have seen around the Report often talk about the system as one combined OASDI system and trust fund. In reality, it’s two separate and distinct funds.

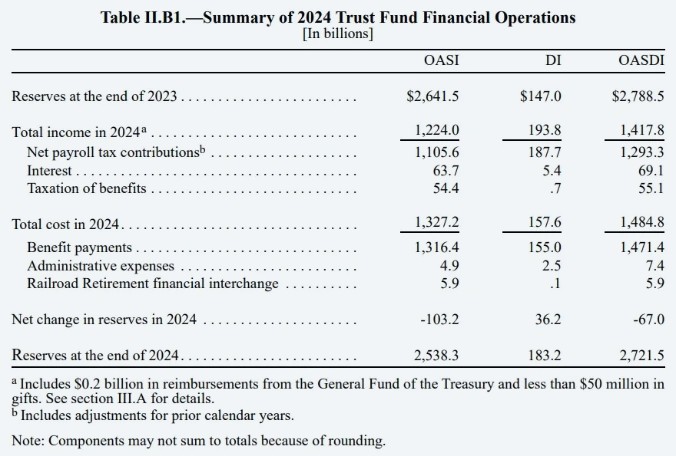

Here are the summarized financial results of the OASI and DI (and combined OASDI) systems for 2024:

I’ll break this down a bit to make it more plain English.

The “reserves” shown in the table are the amounts that were in the trust funds. Or, in my basic example before, you can think of the system’s “reserves” as what it has since accumulated in its bank account.

The OASI system started 2024 with $2.6 trillion dollars in its trust fund. The DI system started 2024 with $147 billion in its trust fund. As such, on a combined basis, the OASDI trust funds had nearly $2.8 trillion of reserves at the beginning of 2024.

The OASI’s total income for the year was $1.2 trillion, $1.1 trillion of which was from payroll taxes paid by workers and their employers. The remaining OASI income was from interest from the U.S. government bonds held in the OASI trust fund, and from income tax collected against OASI benefits paid.

The OASI system’s total expenses for the year were $1.3 trillion, basically all of which were for benefits paid to retirees, their dependents and their survivors. Total administrative expenses attributable to the OASI system were just shy of five billion dollars, and total railroad-related benefit payments made by the OASI system were just under six billion dollars.

In total, the OASI system paid out $103 billion more than it took in, which means it had to tap its trust fund for $103 billion to cover that deficit, causing the OASI trust fund to decrease from $2.6 trillion to $2.5 trillion by the end of 2024.

The DI’s total income for the year was $194 billion, $188 billion of which was from payroll taxes paid by workers and their employers. The remaining DI income was from interest from the U.S. government bonds held in the DI trust fund, and from income tax collected against DI benefits paid.

The DI system’s total expenses for the year were $158 billion, basically all of which were for benefits paid to disabled workers. Total administrative expenses attributable to the DI system were about two and a half billion dollars, and total railroad-related benefits payments made by the DI system were about a hundred million dollars.

In total, the DI system brought in $36 billion more than it paid out, which means it added that much to its trust fund for the year.

As you can see, the OASI system ran at a deficit for 2024 while the DI system ran at a surplus, and their trust funds decreased and increased, respectively.

But, when combined, there was a net reduction in the size the trust fund(s) from $2.8 trillion to $2.7 trillion.

The future of the system and its trust funds

The trustees and the actuaries of the Social Security system make formal projections for the anticipated financial operations and health of the system over the next 75 years. Making projections about the future operations of Social Security is INCREDIBLY difficult, as it involves making educated guesses about things like future birth rates, death rates, immigration trends, marriage and divorce rates, retirement patterns, disability incidence and termination rates, employment rates, productivity gains, wage increases, inflation, interest rates and many other factors.

With that many unknown variables in projecting the future health of Social Security, we know the projections will ultimately be wrong to some extent. But the projections are nonetheless better than not trying to do any forward-looking analysis!

Anyway, as we saw from the 2024 financial summary, the combined system paid out more than it took in for the year. And it’s projected that trend will continue indefinitely. Which means it’s just a matter of time until the combined trust fund depletes.

Per the Report, on a combined basis, the OASDI trust funds are expected to deplete in 2034. However, on a separate basis, the DI trust fund is expected to not deplete at any point in the 75 year projection period. It’s the OASI trust fund that’s strained. Specifically, it’s currently projected to deplete in 2033.

What would actually happen if the OASI trust fund depletes? Going back to the example of the person’s bank account eventually depleting, if/when the OASI trust fund depletes, it doesn’t mean Social Security is going away.

As projected in the Report, if there are never any changes made to the system in terms of how it’s funded or how benefit payments are determined, once the trust fund depletes in 2033, the money projected to come into the OASI system from that point forward would only be enough to cover roughly 77% of all OASI benefits from that point onward.

In other words, if no changes are made the Social Security system and the OASI trust fund does indeed deplete in 2033, EVERYONE will have to have a 23% reduction to their Social Security retirement benefits.

This means that people who are not yet receiving benefits will have a 23% reduction to their eventual benefit compared to what benefit amount is currently projected on the Social Security statements.

However, it also means people who are already receiving Social Security retirement benefits would have a 23% decrease in their benefit starting in 2033.

Since the DI system is projected to remain financially healthy for the indefinite future, there are no projected reductions in Social Security disability benefits; just retirement benefits.

Based on the above and the imminent depletion of the OASI trust fund, it’s obvious that changes need to be made to the system. Clearly something’s got to give, as payments will need to be reduced – potentially precipitously – if no changes are made.

But, should people in or near retirement be concerned about their Social Security retirement benefits getting reduced??? No, not in my opinion.

I think anyone who’s already 62 or older and therefore able to start their Social Security retirement benefits, if they haven’t already, doesn’t need to worry about seeing any topline reduction to their benefit amounts.

My educated guess is that even people who are in their 50s likely don’t have to worry about their benefits getting reduced. However, people younger than 50-ish…expect there will be some form of benefit reduction. Again, this is just my guess.

Recall what I said earlier in the example of the person whose monthly income isn’t large enough to cover their monthly expenses AND they deplete their savings account; they either need to spend less and/or bring in more.

Social Security is no different. Cutting benefits isn’t the only way to fix its recurring deficit; the system can also increase what it brings in.

For example, in the Report, one of the potential solutions it discusses to keep the trust funds funded for the duration of the 75 year projection period without making any benefit reductions is to increase the Social Security payroll tax from 6.2% per employee and employer, to 8.03% per employee and employer. Ultimately, this would be the most clean and direct way to bolster the system without having to dig deeper into the mechanics, formulas or legislation of the system.

However, that level of payroll tax increase presumably won’t happen, as it would be a bit of a shock to increase people’s payroll taxes by 1.8 percentage points. Especially since the increase would be felt disproportionately more by lower wage earners; recall the amount of earned income on which Social Security tax is paid is capped, and currently $176,100 this year. A person making $500,000 in wages doesn’t pay any more into Social Security than someone with $176,100 of wages. However, for what it’s worth, that also means the higher wage person won’t necessarily get any more out of Social Security than the person with $176,100 of income.

There are other ways within the current structure of the system to increase the income into it beyond just increasing the payroll tax contribution rate. For example, the wage cap can be increased or removed, or more of Social Security could be treated as federally taxable. Or, the Social Security system could have a larger overhaul that introduces some other form of income that doesn’t yet exist in the current system.

As for reduction of payments, in my opinion, that definitely won’t be a sweeping reduction across everyone. Instead, I firmly feel people in or close to Social Security retirement benefit age will be spared any topline reduction to their benefits. They may see more of their benefits taxed, which would ultimately reduce the net amount of benefit taken home, but it wouldn’t be a gross reduction per se, which is what I mean when I said I don’t foresee any “topline” reductions.

Or, perhaps the annual inflation increases on benefits could be reduced, thus resulting in a payment reduction in the sense that people’s inflation-adjusted growth in benefits will be less than it otherwise would have been.

Or, the age at which people reach “Full Retirement Age” and can claim an unreduced benefit can be increased. This happened in the past and therefore, in my opinion, is likely to happen again. Before the 1980s, Full Retirement Age for everyone was 65. But, starting in the 1980s, there was a gradual phasing in of older Full Retirement Ages; first 66, then ultimately 67. And that change didn’t immediately impact people. For example, someone who was 60 at the time the changes were put into place didn’t see any increase to their Full Retirement Age, and therefore didn’t see any reduction to their expected benefit amount. Instead, people who were at the time decades away from their 60s had their Full Retirement Ages increased, thus giving them ample time to plan and adjust accordingly.

Also, deep within the formula for calculating one’s Social Security benefit are multiple components that could each potentially be tweaked to reduce the amount of eventual retirement benefit people will receive.

Final thoughts

All said and done, it’s clear the Social Security system – specifically the OASI system; not the DI disability system – is unsustainable and something’s got to give. And there is no reason to think changes won’t be made to the system to strengthen and bolster it before the OASI trust fund depletes in approximately eight years.

However, considering any and all changes will need to be some combination of having people pay more in and/or get less out, most politicians appear to not want to touch it and risk using up any political capital and goodwill they may have. Or at least, they don’t want to do so until the 11th hour when they will no longer have the ability to further kick the can down the road.

While we don’t yet know what final change or changes will be made to shore up the system, my guess is it will be a combination of relatively small changes, as opposed to just one comparatively larger change. And it will almost certainly include some combination of having people pay more in and get less out. BUT, I firmly believe anyone who’s currently 50-ish or older doesn’t need to worry about seeing any topline reduction in their retirement benefits. That would be political suicide for any legislator who support it. In my opinion, expect any reduction in benefits to impact people who are still a couple decades or more away from being able to get benefits.