The optimal time to claim Social Security

One of the most common questions retirees have is, “when is the best time to claim Social Security?” For better or worse, the answer is a resounding “it depends!”

Social Security is the income foundation of most peoples’ finances in retirement. It’s guaranteed to last as long as you do, and it has an inflation-based Cost of Living Adjustment, or “COLA,” every year. As such, the amount of benefit you receive will increase over time as inflation inevitably occurs (and, in case you’re wondering, your benefit won’t decrease if there is deflation).

With that said, getting the Social Security claiming decision right can be one of the most impactful decisions you can make in your retirement planning. However, there often isn’t a definitively “right” time to claim Social Security. There are a lot of factors and variables to consider. Unfortunately, many of those factors and variables involve making educated guesses about the future. I’ll explain what I mean by that. But first, I want to give a quick overview of the retirement benefits Social Security provides.

Most people who work (whether as an employee for someone else, or self-employed) mandatorily pay a portion of their earnings in “payroll” taxes. These payroll taxes are also known as Federal Insurance Contributions Act or “FICA” taxes, which are taxes to fund the Social Security and Medicare systems. I say most people pay them, because some don’t. Specifically, about ¼ of state and municipal employees don’t pay into Social Security, which means they aren’t eligible for their own Social Security benefits as a result.

The amount of Social Security retirement benefit you’re ultimately eligible for is based on your highest 35 years of earnings. Specifically, each year of earnings prior to the year you turn 60 is indexed for inflation, from the year the earnings were earned, up to the year you turn 60. Any earnings in the year you are 60 or older are not indexed for inflation; they’re taken at face value. Of this entire inflation-indexed earnings history, the highest 35 years are used to determine your Social Security benefit.

There is much more to the benefit calculation than this, and all of the gory details are beyond the scope of this article. However, if you’re interested in getting your hands dirty with the topic, I made a video Calculating Your Social Security Primary Insurance Amount that walks through the process and formula in detail. Enjoy!

Anyway, the benefit calculated from your highest 35 years of inflation-indexed earnings is technically called your Primary Insurance Amount, or “PIA.” That represents the amount of monthly Social Security retirement benefit you’d receive if you start your benefit at your Full Retirement Age, or “FRA.”

What’s FRA you ask??? Good question. It’s important to know your FRA is not tied to when you actually stop working. It’s simply a measure that exists solely for the purposes of Social Security, whether or not you’re actually “retired.”

If you were born in 1960 or later, your FRA is 67. If you were born between 1943 to 1954, your FRA is 66. If you were born between 1955 and 1959, your FRA is somewhere between 66 and 67. Specifically, if you were born in 1955, your FRA is 66 and two months. If you were born in 1956, your FRA is 66 and four months. If you were born in 1957, your FRA is 66 and six months. Etc…keep adding two months for each additional birth year up to 1960.

If you were born prior to 1943, I’m assuming you’re probably not reading this article. And even if you are, you’re already beyond the maximum Social Security claiming age of 70, so I won’t bother going into the FRA details, as I assume you already started your benefit.

So, if FRA doesn’t mean anything other than it’s the age at which you’d get your PIA if that’s when you start your Social Security retirement benefit, why bother bringing it up??? Another good question!

It matters because the amount of monthly benefit you actually receive could be more or less than your PIA, depending when you start your benefit.

If you start your benefit before your FRA, it will be less than your PIA. If you start your benefit after your FRA, it will be larger than your PIA. All else equal, the sooner you start it, the smaller it will be. And vice versa.

You can start your benefit as early as age 62, but it will then have the largest reduction from PIA. Conversely, you can delay the start of your benefit until as late as age 70. If you start your benefit then, it will have the largest increase from your PIA. You can technically wait to start your benefit later than age 70, but you’re almost certainly leaving money on the table by doing that, as your benefit will no longer increase beyond age 70 (other than from the annual COLA adjustment, which you’d get anyway even if you started your benefit).

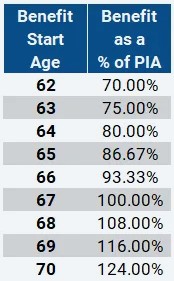

Below is a summary of the reductions from PIA, or increases to PIA, to starting your Social Security retirement benefits at an age other than your FRA. This chart assumes you were born in 1960 or later, thus your FRA is age 67.

To put some numbers to this, assume your PIA is $2,000 per month. If you start your benefit right at your FRA of 67, you’d get $2,000 per month in Social Security (plus the annual COLA adjustments going forward).

If you waited until age 68 to start your benefit, it would be 8% higher than your PIA, which means it would be $2,160 per month. If you started your benefit at age 66, it would be reduced by 6.67%, which means a benefit of $1,866.67 per month. In both cases, you’ll get the annual COLA increase each year going forward.

For simplicity sake, I showed the benefit reductions or increases assuming you start your benefit in the month of your birthday; such as in the month you turn 62, or the month you turn 63, etc. In reality, you can start your benefit at any time, in any month in between birthdays.

The reductions and increases from PIA are actually calculated on a monthly basis. For example, if you start your benefit any point up to three years before your FRA, the reduction is 5/9% per month. Or, if you start your benefit any point after your FRA, the increase is 2/3% per month.

Now that you know your benefit is smaller the sooner you start it, and larger the longer you wait to start it (up to age 70), we can finally start to talk about optimized claiming strategy…yay!

Many people view the Social Security claiming decision as a pure break-even analysis; obviously waiting to start to get a larger benefit is nice BUT that means you forego getting all of the months of benefits along the way. And vice versa; starting your benefit as soon as possible means you’ll start getting benefits sooner than if you delay BUT those benefits will be lower for the rest of your life than they otherwise would be if you delay.

Basically, if you knew with certainty when you were going to die, it would be substantially easier to know when to start your Social Security such that you maximize how much you’ll get over your lifetime. For example, if you’re currently 62 and you just received a terminal diagnosis such that you’re not expected to live more than another year, you’d probably want to start benefits as soon as you can instead of delay. Or, if you knew with certainty you’d live to 100, you’d probably want to delay your benefits until age 70 to make them as large as possible so that you have that much larger of a benefit for those next 30 years.

The math is such that if you were to delay your benefit all the way until age 70, the break-even age you’d have to live to in order to have ultimately gotten more out of Social Security than if you started early is early-to-mid-80s. In other words, if you’re certain you’ll live at least until your mid-80s, you’ll ultimately get more out of the larger benefits from age 70 onward than if you were to have started your benefit early and received more benefits but at smaller amounts each month. And vice versa; if, for example, you know you’re not going to live beyond your late-60s, you’d probably want to start your benefit as soon as you’re able to.

So far it sounds easy, right? Other than having to try to guess when you’re going to check out of this world, there so far doesn’t appear to be much else to consider beyond the basic break-even age I mentioned above. But like all cheesy infomercials say, “wait, there’s more!”

If you have a spouse, a minor child or a permanently disabled child, they may be eligible to get “ancillary” benefits off of your retirement benefit. In other words, whether or not they ever worked and paid into the Social Security system themselves, they may be eligible for benefits off of your earnings history and their relationship to you. And I should mention that even if/when others are pulling ancillary benefits off of your Social Security record, that doesn’t reduce the amount of benefit you’re still able to get for yourself.

For your spouse, minor child or permanently disabled child to get benefits off of your record while you’re alive, you first need to start your own benefit. This means the simple break-even approach isn’t so simple anymore; you no longer have to consider the length of time YOU may be getting benefits, but you now also have to consider how much ancillary benefits may be paid to others off your earnings history.

For example, maybe you’re single and have a permanently disabled child. Even if you think you are likely to live well beyond the average life expectancy of mid-80s, it may be more beneficial to start your benefit early so your child can then start getting ancillary benefits off your record. You basically now need to consider the strategy that will maximize the expected aggregate lifetime benefits paid to you AND your child. This definitely complicates the analysis…

In addition to paying ancillary benefits to others while you’re alive, there are also potential “survivor” benefits payable to your spouse, minor child and/or permanently disabled child after your passing. For purposes of this article, I’ll only talk about survivor benefits in the context of spouses. Survivor benefits for minor and/or permanently disabled children is an additional level of complexity I’m choosing to keep out for the sake of article length!

For married couples, when one spouse dies, the smaller of the two spouse’s benefits basically falls away and the larger of the two benefits lives on - plus the annual COLA adjustment - for the life of the surviving spouse.

For example, assume Spouse A has a monthly benefit of $4,000 off his or her own earnings history, and Spouse B has a monthly benefit of $2,500 off his or her own earnings history. Regardless which spouse dies first, the $4,000 per month - plus annual COLA - will live on for the life of the survivor, while the other $2,500 will effectively stop.

Basic decision framework for Single vs Married

Let’s now start to put some basic decision-making framework to the claiming decision. I’ll keep it really simple for now, and assume there are two scenarios:

1. A single person with no minor or permanently or disabled children

2. A married couple with no minor or permanently disabled children

For single persons, the basic break-even approach is a good starting point in deciding when to start Social Security. Simply put, if you have good reason to believe you’ll live beyond your mid-80s, it’s likely prudent to delay your benefit as long as possible; i.e. until 70. Or, if you think you’ll live a shorter than average life, start sooner rather than later. Exactly how soon??? It’s really hard to say without knowing exactly when you’ll leave this realm. However, I’m inclined to say if you don’t think you’ll make it to your 80s, might as well start as soon as you can. Guessing life expectancy isn’t an exact science, unfortunately.

For married persons, the basic rule of thumb is that the person with the larger benefit delay as long as possible; i.e. 70. The person with the lower benefit would start sooner. This is the tricky part; how much sooner??? Again, there unfortunately isn’t an exact science to it. I think targeting to start around 65-67 is plenty defensible. But if you wanted to start early, I can’t say that’s a bad idea.

The more important aspect of the decision for a married couple is that the person with the larger benefit delay as long as possible. That’s because of the survivor benefit aspect for married couples. By maximizing the higher of the two benefits, you’re ensuring that the higher benefit will live on for whomever ends up outliving the other.

If you assume one spouse will predecease the other (as opposed to both spouses dying at the same time), you’re assuming the smaller of the two benefits will fall away upon the passing of the first spouse. And the higher of the two benefits will live on for the survivor. For that reason, there should generally be less impact or importance to when the person with the smaller benefits starts theirs.

And, in case you’re wondering, even if the spouse with the larger benefit dies before actually starting their benefit, the survivor will still benefit from getting whatever that benefit would have been had it hypothetically started when the deceased died. For example, assume the spouse with the higher benefit dies unexpectedly at 69 and was delaying their benefit until 70. The survivor benefit for the surviving spouse would be whatever the deceased’s benefit would have been when they were 69, even though they hadn’t actually started their benefit before passing.

Keep in mind rules of thumb are just that; rules of thumb. The big exception to the above rule of thumb for married couples (i.e. that the spouse with the higher benefit delay as long as possible, while the other spouse start earlier) is if both spouses have shorter than average life expectancy. In that case, both spouses should arguably start their benefits early. But exactly how early??? That’s hard to say without knowing exactly when both people will check out of this world.

Other important considerations

While the basic break-even approach mentioned above is a good starting point for considering when to start Social Security, it’s unfortunately not that simple.

There are other considerations which may come into play, such as:

Starting benefits before FRA while still working – if you start ANY benefits (i.e. either your own, an ancillary spousal benefit or a survivor benefit) prior to your own FRA and you are still earning wages or have self-employment income, the amount of monthly benefit you receive may be reduced.

If you’re younger than the year of your FRA and you have more than $22,320 of earnings in 2024, your monthly benefit may be reduced $1for every $2 over that limit. If you’re in the year of your FRA - but not actually yet FRA - the earnings limit is higher, at $59,520 for 2024. Your benefit may be reduced $1 for every $3 over that limit.

All else equal, if you’re still working, it may not make sense to start your benefit prior to your FRA.

Tax Planning– there are potentially a lot of moving parts here that could lead to benefitting from delaying benefits.

A common example is if you have a lot of pre-tax money in traditional tax-deferred accounts such as IRAs or 401(k)s. If you retire in your late-50s or early-60s, your earnings will stop and your taxable income will drop substantially. And if you do not yet start Social Security or turn on any pensions or annuities you may have, you can potentially have a REALLY low income tax situation in those years. Perhaps you’d only have some bank account interest, and maybe some dividends from a brokerage account.

These low income years can be a great opportunity to realize tax on your pre-tax money by taking out distributions and/or doing Roth conversions. This window of opportunity could be the lowest tax rate you’ll ever be in for the rest of your life. As such, it could be a really tax-efficient way to get money out of your pre-tax accounts. Knowing you’ll have to eventually take money out of them - and pay tax on it - in the future when Required Minimum Distributions (“RMDs”) start, why not get ahead of it and do so while paying lower taxes than you will in the future???

The other tax planning benefit to pulling forward income from pre-tax account to delay Social Security is that Social Security is a more tax-advantaged source of income that distributions from pre-tax accounts like IRAs or 401(k)s. That’s because, at most, no more than 85% of Social Security is taxable at the federal level. Whereas with pre-tax account distributions, 100% of them are taxable.

Also, at the state level, most states don’t tax Social Security at all, whereas most states do tax pre-tax retirement account distributions (though there are exceptions, like IL and PA, and the handful of states that don’t have income tax in the first place).

All else equal, over the long-term, it would likely be better from a tax-efficiency standpoint to get more of your income from Social Security as opposed to distributions from pre-tax retirement accounts. Delaying Social Security and trimming down your pre-tax account balances in the process could help achieve that.

While this article sums up the key considerations to have in mind when making your Social Security claiming decision, it’s possible there could be other unique circumstances that could impact your decision. If nothing else, there could be emotional and subjective factors that influence you.

For example, maybe you’d really struggle emotionally with the notion of not getting a guaranteed “paycheck” as soon as you stop working and your prior paycheck goes away. While the math and objective factors may say you should delay the start of Social Security as long as possible, perhaps you’d lose sleep and get agita from not starting Social Security ASAP. In that case, starting early could be the right decision for you.

In my opinion, one factor that should NOT be taken into consideration is opinion and speculation about a potential reduction in benefits due to possible cutbacks in the Social Security system. While anything is hypothetically possible, I can’t picture a scenario where people who are of Social Security age or close to it (i.e. 50-something or older) would see an actual reduction in benefits.

As such, in my opinion, the “I want to get mine before it gets reduced” mentality is flawed and misplaced. Even if your benefit is to eventually get reduced, starting it early would just be doing yourself harm by getting less benefit in the first place, let alone ALSO having a reduction in the future. That would be a double whammy of less benefit.

As you can see, there is rarely, if ever, a simple and undeniably “right” claiming strategy for starting Social Security. But hopefully this article give you good food for thought to help at least make a well-informed educated guess of a decision. After all, deciding when to start your benefit really is nothing more than an educated guess. However, if you at least know the main factors to take into consideration, your guess will be that much more educated!

Disclaimer:

None of the information provided herein is intended as investment, tax, accounting or legal advice, as an offer or solicitation of an offer to buy or sell, or as an endorsement, of any company, security, fund, or other securities or non-securities offering. The information should not be relied upon for purposes of transacting securities or other investments. Your use of the information is at your sole risk. The content is provided ‘as is’ and without warranties, either expressed or implied. Tenon Financial LLC does not promise or guarantee any income or particular result from your use of the information contained herein. Under no circumstances will Tenon Financial LLC be liable for any loss or damage caused by your reliance on the information contained herein. It is your responsibility to evaluate any information, opinion, or other content contained.