Understanding how Social Security is taxed

Last month’s article was about how to optimize the Social Security retirement benefit claiming decision. With Social Security on my mind, I figured it would be good to use this month’s article to explain how Social Security benefits are taxed.

Yes, Social Security benefits are potentially taxable (notice I said potentially…more on that later).

The bulk of this article will be about the federal income tax treatment of Social Security. However, it’s important to note that some states also tax Social Security.

First, a handful of states don’t have any income tax at all (such as Florida, Texas, etc.) As such, those states don’t tax Social Security.

As for the states that do have an income tax, the majority explicitly exclude Social Security benefits from being taxable at the state level.

As of 2024, there are only nine states that potentially tax Social Security at the state level: Colorado, Connecticut, Kansas, Minnesota, Montana, New Mexico, Rhode Island, Utah and Vermont.

Thankfully though, even if you live in one of these nine states, it’s possible that some or all of your Social Security might not actually be taxed at the state level.

For example, Colorado lets people 65 or older exclude all of their Social Security from taxation. And people between 55 and 64 can exclude up to $20,000 of Social Security from taxation.

Okay, that’s it for state income tax. Let’s now move on to the federal tax treatment of Social Security. This is where things get fun!

At a super high level, the key takeaway is that no more than 85% of your Social Security benefits may be included in your taxable gross income on your federal tax return. That doesn’t mean you’ll pay tax of 85% on your benefits; it means that no more than 85% of your benefits may be subject to whatever tax rate you have to pay on your taxable income.

But here’s where things get tricky; the actual amount of your Social Security benefits that gets included in your gross income can range anywhere from zero to 85%. And the formula to figure out the exact percentage is rather convoluted and generally not something you can do with just a pencil and paper. Or even with a spreadsheet, unless you know the formula intimately well and are able to build it into the necessary series of “if this, then that” formulas in spreadsheet software.

It's not impossible to build out the formula yourself. But, for the majority of people, the only practical way to know for sure how much of your Social Security benefits are going to be federally taxable is to run through a full mock (or actual) tax return using some kind of tax prep software. Or an online tax return simulator like the ”Dinkytown” 1040 calculator here.

While I can’t easily break down the full formula here in this article, I’m going to at least summarize the key points and show some samples to give you a rough idea of the approximate level of how much Social Security is taxable under a few different scenarios.

However, for those of you who want to see the full calculation in all of its gory details, check out the “Social Security Benefits Worksheet” in the Instructions to Form 1040. Specifically, for the 2023 Instructions to Form 1040, the Social Security Benefits Worksheet is on page 32. (The 2024 instructions are not out yet, but there shouldn’t be any substantive changes)

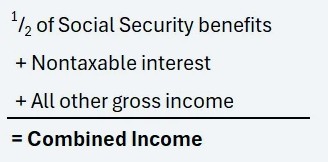

In a nutshell, the amount of your Social Security benefits that is federally taxable is a function of how much total income you have. But it’s not just any old measure of income that’s used. You have to look at a special measure of income called “Combined Income.”

Combined Income is a figure that’s used solely for the purposes of determining how much of your Social Security is taxable; it has no relevance or usage anywhere else in your tax return.

Your Combined Income is equal to:

It’s important to note that the “½ of Social Security benefits” is ½ of your GROSS benefit amount; not ½ of the amount you get after Medicare premium deductions and/or federal tax withholdings.

“Nontaxable interest” is the figure reported on line 2a of your Form 1040 tax return. Interest from municipal bonds held inside normal non-qualified brokerage accounts is typically the only item that would be reported on line 2a.

The ”All other gross income” is as the name implies; essentially all other gross income reported on your tax return (e.g. wages, taxable interest, dividends, pension and annuity income, capital gains and the “additional income” reported on Schedule 1). Note that this is not simply your “Adjusted Gross Income” from your tax return. It’s instead a manually calculated separate figure of other gross income.

Here's a basic example of Combined Income: Assume you receive $24,000 of gross Social Security benefits, $500 of nontaxable interest from municipal bonds and $30,000 of pension income. Your combined income would be:

½ of $24,000, or $12,000 + $500 + $30,000 = $42,500

So, why do you need to know your Combined Income??? Because that’s the first step in figuring out how much of your Social Security benefits may be taxable.

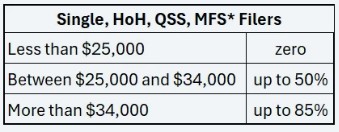

Specifically, there are Combined Income thresholds that set limits of how much of your benefits may be taxable.

If you file a tax return as Single, Head of Household, Qualifying Surviving Spouse or Married Filing Separately*, here are the different Combined Income thresholds and the respect percentages of your Social Security that may be taxable:

*Note that if your filing status is Married Filing Separately, you must have lived apart from your spouse for the ENTIRE year, otherwise 85% of your benefits be taxable, regardless of your Combined Income.

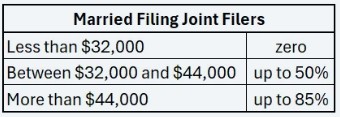

If you file a tax return as Married Filing Joint, here are the thresholds and respective taxable percentages:

Like I mentioned before, the actual formula to determine exactly how much of your benefits is taxable is a bit clunky to try to spell out in detail here. But I figured I’ll show some sample scenarios to give you an idea of how much of the person’s Social Security benefits is federally taxable in each case.

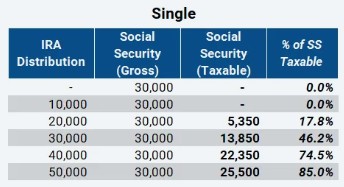

First, let’s look at a Single filer. I’m assuming the person has $30,000 of gross Social Security benefits. And I’m assuming the only other source of income the person has is IRA distributions. I’m showing six different scenarios, where the only difference is how much IRA distribution the person is taking; ranging from zero to $50,000, in increments of $10,000:

As you can see, all else equal, the higher the amount of the IRA distributions, the larger the portion of the person’s Social Security that’s taxable.

Look at the third row, for example. The person’s Combined Income is $35,000 (1/2 of the $30,000 of Social Security + $20,000 of IRA distribution). This is in the top band of Combined Income for Single filers (i.e. more than $34,000 of Combined Income). Yet, their Social Security isn’t 85% taxable; it’s only 17.8% taxable.

It's not until the last scenario where the person’s Combined Income is $65,000 (1/2 of the $30,000 of Social Security + $50,000 IRA distribution) that 85% of their Social Security is taxable.

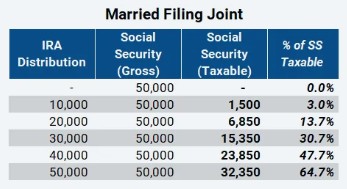

Let’s look at a similar analysis, but this time for a Married Filing Joint couple:

In this scenario, I’m now assuming the couple’s combined gross Social Security income is $50,000. And, like in the case of the Single person, I’m again assuming IRA distributions between zero and $50,000, in increments of $10,000.

You can see that even with $75,000 of Combined Income (1/2 of the $50,000 of Social Security + $50,000 of IRA distribution), the couple’s Social Security still isn’t 85% taxable; it’s only 64.7% taxable. This helps reiterate that it’s “UP TO” 85% of benefits may be taxable when Combined Income exceeds the top threshold shown in the previous tables.

I should also add that just because some of your Social Security is taxable doesn’t mean you actually have to pay tax on it. Wait, what??? Yep, you heard that correctly!

That’s because the amount of Social Security that’s taxable is simply included in your Adjusted Gross Income on your tax return. But that’s not the amount on which you pay tax. You pay tax on your TAXABLE Income.

For most people, they use the “Standard Deduction” on their tax return. Basically, Taxable Income on which you pay tax is equal to your Adjusted Gross Income minus your Standard Deduction.

For a Married Filing Joint couple in 2024, the Standard Deduction is $29,200. With that in mind, let’s look at the third scenario in the Married Filing Joint table above:

The couple’s Adjusted Gross Income would be the $20,000 of IRA distribution + the $6,850 amount of taxable Social Security benefits = $26,850.

Since their Standard Deduction of $29,200 is larger than their Adjusted Gross Income of $26,850, their Taxable Income would be zero, meaning they would have no federal tax obligation for the year. As such, even though some of their Social Security is taxable, they don’t actually have to pay any tax. Wild stuff, I know.

That’s it for now. I hope you found this helpful. Again, I wish I could have actually spelled out the actual formula here in this article, but it would have been too clunky to get across cleanly. There really is no substitute for either 1) building out the formula yourself in a spreadsheet or 2) using a tool that already has the formula built in, such as actual tax prep software or an online calculator like the Dinkytown 1040.

Yes, you can look at the Social Security Benefits Worksheet in the Instructions to the Form 1040 to see the formula spelled out, but it doesn’t really help you to visualize it well that way. You have to actually recreate the formula to fully understand and appreciate what exactly it’s doing.

Social Security is a tremendously complicated system. With that said, it sadly isn’t surprising that the way in which it’s taxed is equally bewildering, for better or worse.

Disclaimer:

None of the information provided herein is intended as investment, tax, accounting or legal advice, as an offer or solicitation of an offer to buy or sell, or as an endorsement, of any company, security, fund, or other securities or non-securities offering. The information should not be relied upon for purposes of transacting securities or other investments. Your use of the information is at your sole risk. The content is provided ‘as is’ and without warranties, either expressed or implied. Tenon Financial LLC does not promise or guarantee any income or particular result from your use of the information contained herein. Under no circumstances will Tenon Financial LLC be liable for any loss or damage caused by your reliance on the information contained herein. It is your responsibility to evaluate any information, opinion, or other content contained.